Some of the world’s most famed investors and the biggest Wall Street banks are voicing a near consensus that Japan’s stock market is the place to be as its larger peers — the US and China — grapple with rising economic headwinds.

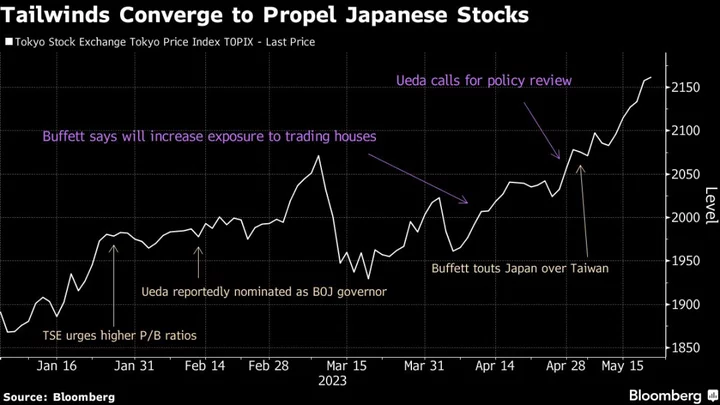

Man GLG, JPMorgan Asset Management and Morgan Stanley are among those who see more upside after Japan’s Topix Index reached its highest level since 1990 this week. Equities are shooting above levels dubbed as the “iron coffin lid” as the return of inflation, improving shareholder returns and an endorsement by Warren Buffett all combine to burnish the appeal of the world’s third-largest stock market.

“Japan is my favorite global stock market at this point. It’s getting everything it’s wished for,” said Jack Ablin, chief investment officer at Cresset Capital Management, a Chicago-based investment advisory firm that manages about $60 billion. “We are about 50% overweight Japanese stocks in our developed-market strategy.”

Japan stands out amid anxiety in the US over the debt-ceiling issue and a possible recession, and as China’s uneven economic recovery and its lackluster market increasingly frustrate global investors. Overseas funds have further boosted their holdings of Japan stocks this month after snapping up 2.2 trillion yen ($15.9 billion) in April, the most since October 2017.

The Topix Index closed at 2,161.69 on Friday, taking its gain in May to 3.8% in dollar terms. The Nikkei 225 has rallied more than 5% and finished Friday at its highest in nearly 33 years. Meanwhile, China’s CSI 300 Index has fallen about 3.5%, continuing to lose ground after the initial reopening rally evaporated. The S&P 500 has added less than 1%.

Jeffrey Atherton, head of Japanese equities at Man GLG, sees further 10-15% potential for the market on resilient earnings, modest valuations and corporate reforms. Man GLG is one of the investment divisions of Man Group Plc, the world’s largest publicly traded hedge fund.

“We expect Japanese interest rates to remain very low by global standards, so monetary policy should be supportive to risk assets, unlike other regions,” he added.

Japan’s market value has surged about $518 billion since a Jan. 5 low, data compiled by Bloomberg show. Japan equity funds lured $800 million in the week ended May 10, the most in seven weeks, while those in the US and Europe saw outflows, according to EPFR data.

All of this comes as years of loose monetary policy finally translates into higher inflation. Consumer prices excluding fresh food rose 3.4% from a year ago in April, showing that Japan has put deflation firmly behind without stoking excessive price gains that warrant rate hikes like in the US. China, on the other hand, is facing deflationary risks.

Having long sat on piles of cash, Japanese companies are also coming to terms with the need to improve shareholder returns and untangle cross-shareholdings in response to growing demand for better corporate governance.

Share buybacks hit a record in fiscal 2022, with investors expecting more following the Tokyo Stock Exchange’s call in January to boost valuations for firms trading at a book value ratio of below one.

“We are beginning to see the interests of all shareholders being recognised,” said Alex Stanić, head of global equities at Artemis Investment Management. “Too many Japanese companies have been trading for too long at a discount to their book value. That makes for great bargains for investors.”

Warren Buffett helped fuel the recent optimism toward Japan by renewing his endorsement for the market during a trip earlier this year. Societe Generale SA and Pictet Wealth Management are among those with an overweight call on Japan and an underweight on US equities.

Despite the dominant optimism, the market could still suffer pullbacks in the near term as technical indicators show indexes are in overbought territory. Real wages are falling even as inflation picks up, and a slowdown in the global economy could weigh on local exporters reliant on the US and Chinese markets.

Analysts expect Japan’s economy to grow about 1% this year, above the 10-year average. The US and China, at 1.1% and 5.7% respectively, are forecast to expand below their historical trends.

For many investors, it’s Japan’s valuation that is too cheap to ignore. Almost half of TSE Prime Market Index members are trading below book, compared with just 5% of the S&P 500 Index, data compiled by Bloomberg show. Even after the rally, the Topix’s price-to-book ratio is about 1.3 times, in line with its 10-year average.

“Despite strong performance year to date, majority of the sectors are still at large discount to the S&P, which makes valuations appealing,” said Evgenia Molotova, senior investment manager at Pictet Asset Management in London. “We believe Japan will continue to demonstrate strong performance in the medium term.”

--With assistance from Hideyuki Sano and Sagarika Jaisinghani.

Author: Ishika Mookerjee, Winnie Hsu and Elena Popina