By Winni Zhou and Rae Wee

SHANGHAI/SINGAPORE China's heavily managed yuan has dropped to multi-month lows and breached the closely watched 7-per-dollar level, and analysts who are predicting more weakness point to the U.S. Federal Reserve's policy as being the bigger driver than economic weakness at home.

The yuan, also referred to as the renminbi, hit 7.0234 per dollar on Thursday, levels last seen in December before euphoria over China's reopening after the COVID-19 pandemic lifted it for a few weeks.

As doubts grow about the strength of its economic recovery, foreign money has left China's markets and the currency has fallen 4% against the dollar since late January.

Analysts at Nomura and Societe Generale say the yuan could soon head for 7.3, which as last plumbed in November. Kiyong Seong, lead Asia macro strategist at Societe Generale, says a wider monetary policy divergence between China and the U.S. coupled with lacklustre Chinese growth would result in a weaker yuan.

"An important part of the climb in dollar-yuan over the past month has to do with the dollar, so this is not just a renminbi story," said Alvin Tan, head of Asia FX strategy at RBC Capital Markets in Singapore.

Reflecting that, the trade-weighted CFETS basket against which the People's Bank of China (PBOC) manages the currency, has dropped to 99 from 100 in February.

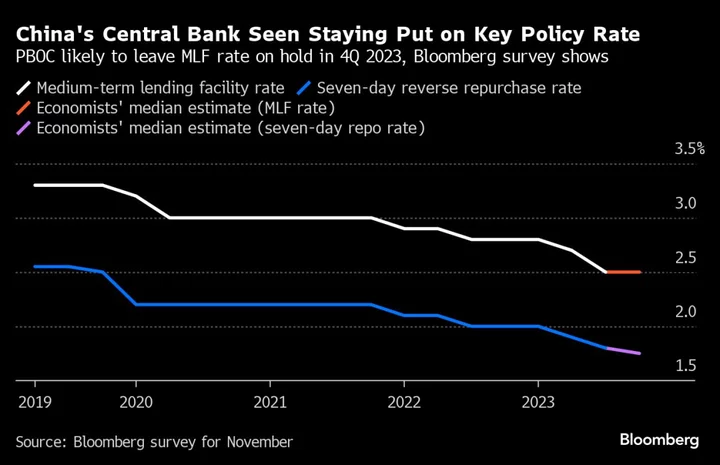

Meanwhile, as the Fed weighs whether to pause its tightening after taking rates up 5 percentage points since March 2022, China appears set to keep monetary conditions loose amid growing signs its recovery is losing steam.

In the forwards market, the wide yield difference has the yuan trading stronger, thus disincentivising exporters to convert their earnings. Six-month yuan is trading at 6.89.

A Shanghai-based exporter, who didn't want to be quoted by name, said he was keeping his dollars for now, rather than swapping them for yuan.

"I know I shouldn't be too greedy, but the yuan will weaken to 7.3. I will wait," he said.

The PBOC has so far given little hint it is uncomfortable with the currency's recent moves or stepped in to defend it. But the RBC's Tan said authorities will be keen not to let the selling accelerate.

"So even if it's weaker, they prefer that it'd be orderly. And frankly, it has been generally orderly so far," said Tan.

The PBOC did not immediately respond to Reuters request for comments.

THE CHEAP CURRENCY

Becky Liu, head of China macro strategy at Standard Chartered Bank, expects the yuan will continue to depreciate.

"The interest rate gap remains wide, so many hedge funds continue to use yuan as a funding currency," Liu said.

"Apart from the carry trade, the other is seasonality as the dividend payment season will start soon. So in the short term, we don't think the yuan has huge upside room, instead we think it will face some pressure."

Analysts at Nomura estimate mainland China firms listed and paying dividends in Hong Kong will make roughly $8 billion of dividend payments in each of June and July 2023.

The usual tailwinds for the yuan from capital inflows are also are flagging as exporters hold back flows and foreign investors hesitate to buy into the market until they are convinced of more solid economic momentum and regulatory support.

While foreign net buying of Chinese stocks has been around 193 billion yuan ($27.92 billion) so far in 2023, they have sold 226.5 billion yuan worth of bonds in the first four month of this year, according to Reuters calculations based on official data.

A look at commercial banks' foreign exchange operations shows they are selling more dollars on net. They sold $9.8 billion to their clients in the four months of this year, according to State Administration of Foreign Exchange.

Yet, foreign exchange deposits grew $28 billion so far this year to $881.9 billion at the end of April, PBOC data shows.

($1 = 6.9121 Chinese yuan renminbi)

(Additional reporting by Jason Xue in Shanghai; Writing by Vidya Ranganathan; Editing by Kim Coghill)