By Yoruk Bahceli and David Milliken

LONDON Britain's government bond market has seen its heaviest sell-off since last autumn's "mini-budget" crisis, lifting two-year borrowing costs to their highest since July 2008 - but investors say there's far less reason for panic than last year, and maybe even a bargain.

Two-year gilt yields hit a peak of just over 4.9% in the first minutes of trading on Wednesday, a day after they had pushed past their previous Sept. 27 high of 4.76%. The bond's price recorded its biggest daily fall since October on Tuesday.

The rapid rise in gilt yields has consequences for the wider economy. British lenders have jacked up mortgage rates in recent days, and the opposition Labour Party has said it may have to slow down green investment plans if it wins power in national elections expected next year due to higher finance costs.

But while the 2.4 trillion pound ($3.0 trillion) gilt market may be back in the headlines for the first since last autumn - when the ructions destabilised pension funds, forced a Bank of England intervention and ultimately cost Liz Truss her job as prime minister - professional investors see few parallels.

Day-to-day moves are much smaller, and mostly affect short-dated gilts where investors are used to price swings as they reassess the outlook for inflation and Bank of England interest rates.

By contrast, September and October's moves were bigger and concentrated on long-dated gilts, some of whose holders were ill-prepared for a sudden drop in value as markets took fright at Truss's plans for tax cuts that ignored Britain's established fiscal rulebook.

"The doom loop we entered into for pension funds hasn't happened this time around," said Jim Leaviss, chief investment officer for public fixed income at fund manager M&G.

"This sell-off is not so much about fiscal stability but about the (interest) rate and inflation environment," he added.

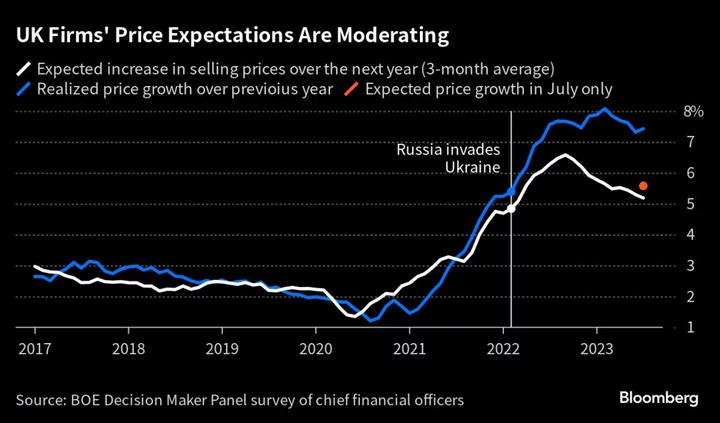

The trigger for Tuesday's slump in short-dated gilt prices was official data which showed basic wages in the three months to April rose at an annual pace of 7.2% - the highest on record outside periods when the data was distorted by COVID furlough payments.

But it was the latest in a string of releases which have shown persistent strong inflation pressure in Britain, despite weak economic growth, and prompted markets to sharply raise their already-high expectations for BoE rates.

Markets on Tuesday priced in a high chance of BoE rates reaching 6% early next year, up from a previous expectation that they would only rise to 5.5% from 4.5%, pushing down the price of short-dated gilts which track expected BoE interest rates.

BoE Governor Andrew Bailey, speaking to a parliament committee on Tuesday, acknowledged that inflation had been slower to fall than the BoE had expected and that the latest labour market data was "very strong".

British consumer price inflation was 8.7% in April, the joint highest with Italy among major advanced economies, and the BoE does not expect it to fall below its 2% target until early 2025.

GILTS UNDERVALUED?

To some investors, gilts now increasingly look a bargain as 6% BoE interest rates appear unrealistic.

"We've been bearish UK government bonds relative to other markets for the last 18 months... but the gilt sell-off is starting to look overdone, and we have got out of this bearish gilt position this week," said Mike Riddell, senior fixed income portfolio manager at Allianz Global Investors.

Two-year gilt yields have risen by 1.1 percentage points this year, compared with a 0.3 percentage point increase for German two-year yields and 0.2 percentage points for U.S. Treasuries.

Raising interest rates to 6% would "succeed in destroying demand" in the wider economy, he said.

While markets price UK inflation at roughly 3% over the medium term, Riddell said some of that reflects the cost of investors paying up for inflation protection, suggesting markets believe inflation will land around 2.5%.

"When compared to other markets, valuations suggest the gilt market is in distress, but there's isn't any tangible distress this time," Riddell added.

PIMCO, one of the world's largest asset managers, also said on Monday that it saw value in gilts and was overweight in some funds.

Ten-year gilt yields now pay an interest rate nearly 2 percentage points higher than the equivalent German government bond. Aside from last autumn's turmoil, this is the biggest premium since the BoE gained operational independence from the government in 1997.

Even if Britain's inflation problem eases faster than markets expect, there are still headwinds for its bond market.

Only around half of gilts' underperformance against U.S. and euro zone bonds reflects Britain's interest rate outlook, with the rest due to other factors such as high debt issuance, according to Barclays fixed income strategist Moyeen Islam.

While the annual gross supply of bonds issued by Britain's government is down from the record highs recorded during the COVID-19 pandemic, it is still hefty at a planned 238 billion pounds for the current financial year.

There is no longer a ready indirect buyer in the form of the BoE's quantitative easing programme. Instead, the BoE is now a seller of gilts, unloading around 10 billion pounds a quarter and not reinvesting the proceeds of a similar volume of gilts which mature.

"There's a dawning realisation about the supply story. There's just no respite from it. And that, plus the rising yield environment, is putting the market under pressure," Islam said.

($1 = 0.7901 pounds)

(Additional reporting by Naomi Rovnick and Dhara Ranasinghe; Writing by David Milliken; Editing by Toby Chopra)