Brazil’s central bank lowered its benchmark interest rate by a larger-than-expected 50 basis points and said future cuts are likely to be of the same magnitude.

Policymakers led by Roberto Campos Neto lowered the benchmark Selic to 13.25% late on Wednesday, as expected by only 11 of 41 analysts in a Bloomberg survey. Thirty others forecast a smaller reduction of 25 basis points. The decision was split, with four board members voting for the smaller quarter-point cut.

“If the scenario evolves as expected, the Committee members unanimously anticipate further reductions of the same magnitude in the next meetings,” policy makers wrote in a statement accompanying their decision. “It judges that this pace is appropriate to keep the necessary contractionary monetary policy for the disinflationary process.”

Brazil’s surprising decision comes just days after Chile cut rates by more than economists expected. Mexico and Peru are expected to embark on similar easing campaigns by the end of the year. Meanwhile, developed economies that were late to fight inflation are not out of the woods yet. Last week, the Federal Reserve and the European Central Bank both left the door open for additional rate hikes.

Read more: Fed Loses to Hyperinflation-Scarred Brazil in Race to Cut Rates

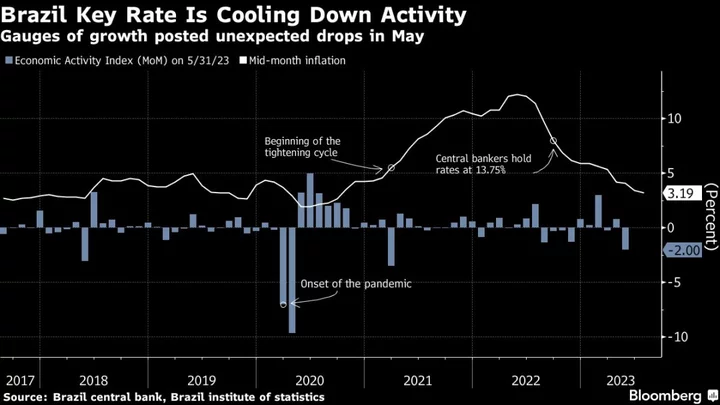

Inflation in Brazil is now below the current target, and core price gauges are also improving. Estimates for cost-of-living increases have fallen since the government decision in June to keep inflation goals unchanged, eliminating a source of investor uncertainty. Still, those forecasts remain above target through 2026.

“Central bankers will have to be careful now to not be hasty on their rate cuts, because they risk de-anchoring inflation expectations and ultimately hurting the economy,” Natalie Victal, an economist at asset manager Sul America Investimentos Dtvm, said before the announcement.

Since taking office in January, Lula has pointed to high interest rates as the main obstacle to the nation’s economic prosperity, often singling out Campos Neto in his criticism. Key members of Lula’s Workers’ Party as well as some top business executives have echoed his complaints.

Meanwhile, there has been progress on proposals that can improve Brazil’s fiscal outlook, as congress is expected to resume debate on a bill to shore up government finances and another to overhaul its tax system. Lula’s economic team says the approval of such legislation will clear the way for looser monetary policy, though investors are still gauging their final impact on public spending.

Wednesday’s decision was the first attended by new board member Gabriel Galipolo, who is Lula’s former deputy finance minister and seen by many as the central bank’s next head after Campos Neto’s term ends in 2024.

--With assistance from Giovanna Serafim.

(Updates with central bank statement in first three paragraphs.)