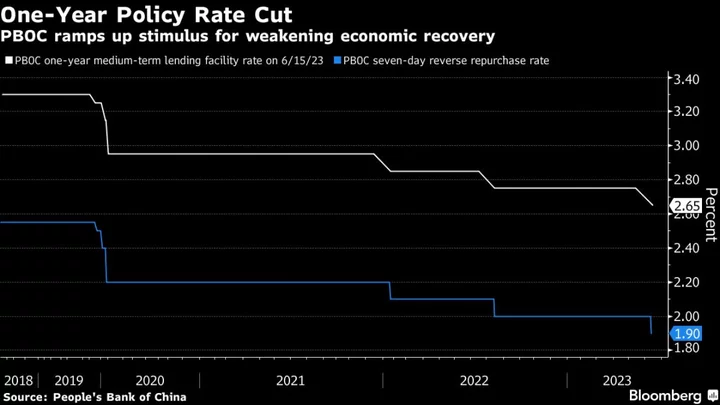

China’s sovereign bonds rallied, while its yuan weakened toward a closely watched-level after the central bank unexpectedly cut a policy rate. Property stocks also gained on hope of more stimulus.

The yield on 10-year government bonds fell four basis points to 2.63%, a nine-month low. The offshore yuan dropped 0.2% to 7.1706 against the dollar, nearing the 7.2 mark, with a similar decline onshore. A Bloomberg gauge of property stocks gained as much as 2.2% before paring.

The People’s Bank of China reduced the interest rate on its seven-day liquidity tool on Tuesday, the first time since August, as economic growth stuttered. Analysts said the central bank may also cut the rate on the medium-term lending facility on Thursday.

Here’s what analysts are saying:

Ju Wang, BNP Paribas head of greater China FX & rates strategy in Hong Kong

- The move confirms the thinking that rates have yet to bottom out, as both producer price inflation and exports are on a downward trend

- Will monitor if there are other policy stimulus coming along with monetary easing soon. Markets expect the rate on the medium-term lending facility and the loan prime rate are likely to be moved too on June 15 and June 20, respectively

- There’s expectations onshore that China may announce measures to support the property sector

- Yuan can weaken further in reaction, but increasingly versus both the dollar and basket. The RMB CFETS basket at 97 is still too high, and a further drop is needed to reduce the deflation pressure locally

Steven Leung, executive director at UOB Kay Hian Hong Kong Ltd.

- “A rate cut is not enough to lift the market, especially when investors have other choices to put their money like in Japan, where the momentum there is so strong,” referring to the equity market

- Market needs to see more policy support, both monetary and fiscal, before turning around the bearish sentiment on China’s economic outlook

Kiyong Seong, Societe Generale lead Asia macro strategist in Hong Kong

- It has been clear that Chinese policy authorities want to have lower interest rates, even at the expense of a weaker currency

- Rate cuts in MLF, LPR will surely follow and China may also reduce the reserve-requirement ratio soon

- As the PBOC rate cut cycle is not over yet, Chinese rate will remain low. The catalyst for a bottoming out in Chinese yields should be from expansionary fiscal policy, but it’s uncertain when that materializes

- Ten-year China yields will fall to 2.6% by year end, while the two-year rate will drop to 1.9%

Khoon Goh, head of Asia research at Australia & New Zealand Banking Group

- With China’s monetary policy going in the opposite direction of the Fed, this will put further pressure on the yuan

- Given the lack of any official comment on the currency or signal from the fixings, today’s rate cut gives the greenlight to push the yuan weaker, with the 7.20 level likely to be tested

--With assistance from Chester Yung.