China has begun a program to allow local governments to swap so-called “hidden” debt for bonds carrying lower interest costs, as it seeks to defuse risks from $9 billion of off-balance sheet borrowing.

The Inner Mongolia region will issue three “refinancing” bonds worth 66.3 billion yuan ($9 billion), with maturities between 3-7 years, the Shanghai Securities News reported, citing an official document.

Bloomberg reported earlier that Beijing will allow provincial-level governments to raise about 1 trillion yuan via bond sales to repay the debt of local-government financing vehicles and other state-owned off-balance sheet debt issuers.

“This means that this year’s special refinancing bond issuance has officially kicked off,” Huachuang Securities analyst Zhou Guannan said, adding that the program will help resolve debt risks in areas with high debt pressure, and more issuances will follow.

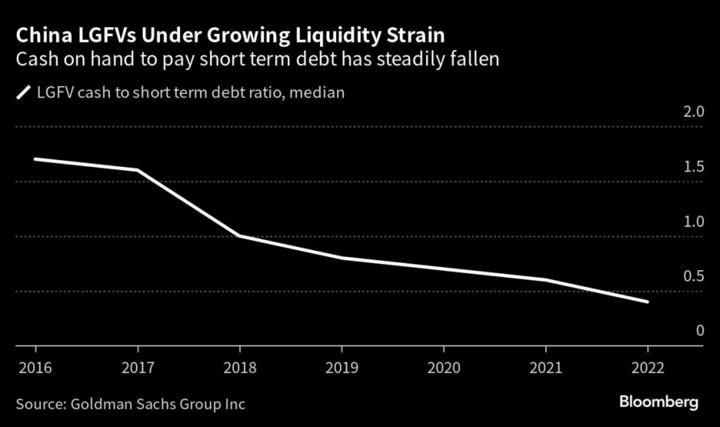

The program is being closely watched because debt servicing costs are increasingly limiting local governments’ ability to deliver fiscal support to the economy, dragging on China’s growth. The risk of an unexpected default by local-government controlled financing vehicles also raises financial stability risks.

Right now is a “good window” for the resolution of debt, given a winding down in the issuance of new local special government bonds, according to a front-page report Thursday in the state-run Securities Times. Beijing wants regions by the end of September to issue their remaining allocation of those bonds, which are mainly used to fund infrastructure, for the year.

The Securities Times report also cited a recent cut by the central bank to the amount of cash lenders have to keep in reserve as another positive development for resolving debt, as that move was intended to keep liquidity ample.

Once the special refinancing bonds are launched, they are bound to be “favored” by more local governments, according to the article.

The large issuance scale of Inner Mongolia’s refinancing bonds, meanwhile, suggests the region either tapped unused quota from prior years or the central government redistributed quota originally intended for other provinces.

The Shanghai Securities News, a state-run newspaper, added that as part of a “special rectification” campaign for hidden debt, a “closed loop” system would ensure that officials are held accountable for debt issuance.

Construction Projects

Chinese local government off-balance sheet debt, or hidden debt, is mostly concentrated in local government financing vehicles (LGFVs), set up to finance construction projects such as roads and social housing.

Such companies, while state owned, often borrow at close to market rates and at short maturities. The debt swap program will shift the debt burden to provincial governments instead but at a lower interest rate and longer maturities.

Bloomberg reported earlier that authorities have identified 12 provinces and cities as “high-risk” areas where more support will be provided — including the provinces of Guizhou, Hunan, Jilin and Anhui, as well as Tianjin city.

The total amount of refinancing bonds planned is small relative to the total amount of LGFV debt which the International Monetary Fund estimates will reach 66 trillion yuan this year.

But the announcement of the scheme has prompted Chinese investors to warm to LGFV debt, with the platforms able to issue a large amount of bonds at lower rates than earlier this year.

Some economists are calling for more to be done. Recent policies on local government debt have been “emergency measures” which haven’t touched on the “core problem,” Xu Gao, chief economist at Bank of China International said in remarks published online this week.

--With assistance from Jing Zhao.

(Adds additional commentary from state media on Thursday.)