China’s local authorities are finding it more expensive to sell bonds, the latest sign of rising stress as policymakers ramp up borrowings to stimulate growth and defuse short-term payment risks.

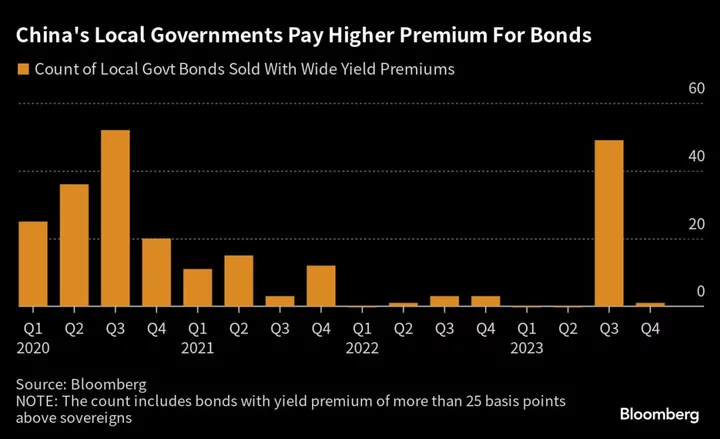

Of the local government yuan bonds sold so far this year, 50 carry coupons with a premium of more than 25 basis points with comparable sovereign debt, according to Bloomberg-compiled data. That’s the most since 2020.

The jump is a departure from the success enjoyed by these borrowers in the past two years, when they had priced almost every note with a yield spread of less than 25 basis points, the lower end of an unofficial band set by regulators. The higher coupons come as local authorities grapple with dwindling land sales and taxation, as a housing-led economic slump persists.

If the demand indigestion worsens, it will heap pressure on the People’s Bank of China to step up liquidity support or ease monetary policy further to fund Beijing’s stimulus plans. On Monday, it add a net 289 billion yuan ($39.6 billion) into the financial system via a one-year policy loan, the most since December 2020.

“Banks are already well fed after absorbing a large amount of local government bonds,” said Liu Lin, deputy general manager of investment banking at Bank of China Ltd. “Pricing may need to better reflect the market dynamics in the fourth quarter.”

Chinese banks owned 83% of the debt at the end of August, the lowest proportion based on Bloomberg-compiled data going back to 2019.

A surge in the debt sales and signs of economic stabilization — raising fears of less easing — have hurt the world’s second-largest bond market in recent months, pushing benchmark sovereign yields to a fourth-month high at one point.

The splurge comes because local authorities had used up over 90% of their special bond quotas for 2023 in the first three quarters, Bloomberg-compiled data show, while sales by the central government also picked up in September.

Debt Deluge

More supply is arriving, including a 1 trillion yuan program to help regional governments refinance hidden debts — a risk that Beijing is keen to reduce. Policymakers are also weighing additional sovereign bond sales of at least 1 trillion yuan for spending on infrastructure, Bloomberg News reported last week.

The Standing Committee of the Communist Party-controlled parliament will meet later this month to review a bill assigning additional local government debt quotas “in advance,” the state-run Xinhua News Agency reported Friday, another move that will allow China to increase the amount local governments can borrow.

Local authorities traditionally exert strong influence on guiding banks to bid at lower yields, said Yang Hao, a fixed-income analyst at Nanjing Securities Co. However, when sentiment weakens, “the low yields become harder to sustain”, he said, adding that demand looks weaker for long-dated notes from fiscally vulnerable regions.

Provinces such as Hunan, Jilin, Jiangxi and Anhui are among those paying higher coupons this year, Bloomberg-compiled data show.

PBOC

To be sure, the chances of defaults by local governments remain slim, even for those with strained finances, said Ding Shuang, chief economist for Greater China and North Asia at Standard Chartered Plc. “If local debt yields deviate too much from those on sovereigns, we would expect some intervention or guidance from government to correct it.”

The nation’s central bank may also be called upon to do more.

The prospect of increased government bond supply means “the PBOC may need to step up its liquidity support and lower interest rates to accommodate the issuance, which adds conviction to our call for another cut to RRR and a policy rate cut in the fourth quarter,” Goldman Sachs Group Inc. analysts including Maggie Wei and Hui Shan wrote in a note, referring to banks’ reserve requirement ratio.

(Updates with PBOC’s liquidity injection in fourth paragraph)