A surge in Chinese sovereign debt issuance is heaping pressure on the central bank to keep funding conditions loose, as authorities pivot toward stronger fiscal stimulus to spur economic growth.

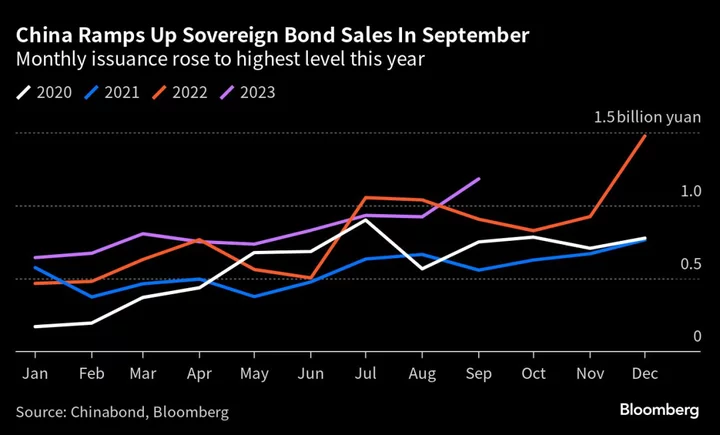

The Ministry of Finance has sold 1.2 trillion yuan ($164 billion) of central government bonds in September, the highest monthly tally in 2023 and 60% higher than the average for the same period in the past three years, Bloomberg-compiled data show. Issuance surged last week after it raised the amount offered for each tenor and added a new five-year note in auctions.

The bond sales boom followed a pledge by China’s finance minister to accelerate spending to bolster a patchy economic recovery, as exports remained weak and a housing slump deepened. The supply increase, which has helped push benchmark government bond yields to a four-month high, also highlights the central bank’s tough balancing act of fostering growth and keeping borrowing costs low at the same time.

“Quickened net financing by the government might be aimed at faster fiscal spending to support the economy” after a lag in both earlier this year, said Ming Ming, chief economist at Citic Securities Co. “There may be an interbank funding gap in October, which may prompt the central bank to step up liquidity support if needed.”

Local governments have also ramped up debt sales to fund infrastructure investment. These, along with early signs of a stabilizing economy and a depreciating yuan, has cooled demand in the world’s second-largest bond market.

The yield on 10-year sovereign bonds rose to its highest since May this week and is on track for its steepest monthly climb since November. In a sign of liquidity pressure in the money market, interest rates on one-year negotiable certificates of deposit, a popular short-term bank debt instrument, also hit a five-month peak this week.

More Liquidity

The People’s Bank of China earlier this month cut the amount of cash lenders must hold in reserve for the second time this year. It also has been injecting cash on a net basis via its money market operation this week.

The debt supply pressure may intensify in the final quarter of the year as a policy focus on generating growth and jobs means leveraging up by China’s central government, whose debt-to-gross domestic product ratio is well below other major economies.

Adding to the risk of indigestion among investors is a likely pickup in the issuance of special bonds for local governments to refinance off-balance sheet debt. In a sign that a 1 trillion yuan program for such purposes has kicked off, the northern Inner Mongolia region is raising 66.3 billion yuan via refinancing notes, the Shanghai Securities News reported.

Citigroup Inc. has recently scaled back its bullish call on Chinese government bonds, with supply concern being one of the key reasons.

“Not only the per-issuance size is now larger than needed to meet the budget, the addition of a new 5-year issuance outside of announced schedule might also increase the likelihood of a larger net bond supply than budget,” the bank’s strategists led by Dirk Willer wrote in a note. Bond auctions by the finance ministry after the Golden Week holiday that starts on Friday will be key to assessing supply pressure, funding implications and whether there will be new off-budget fiscal measures, they added.