A new platform to expand the reach of China’s digital yuan and other central bank digital currencies is moving closer to reality, raising eyebrows among some defenders of a system long dominated by the dollar.

The Beijing-backed digital prototype for sending money around the world without relying on US banks is advancing so quickly that some European and American observers now view it as an emerging challenger to dollar-denominated payments in global finance.

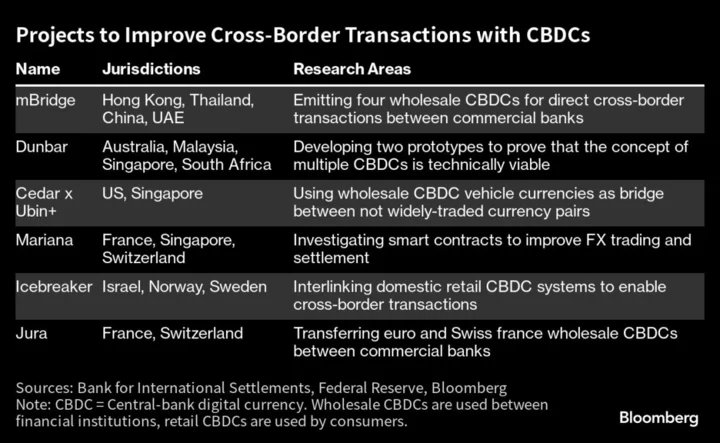

The mBridge project, which is being developed by China, Thailand, Hong Kong and the United Arab Emirates, will likely have a basic working product ready by year-end, four people familiar with the initiative said. It’s a joint effort with the Basel, Switzerland-based Bank for International Settlements — a hub of global central-bank collaboration.

The stakes are enormous. The dollar features in an estimated $6.6 trillion of foreign exchange transactions every day, while half of the approximately $32 trillion in global trade each year is invoiced in dollars, according to BIS and United Nations data. mBridge could eventually make it easier for China’s yuan to be used as a dollar alternative by enabling its digital form to settle large corporate transactions.

While the platform has been under development publicly since 2017, some American and European officials who monitor it are increasingly worried that it’ll help give Beijing a head start using digital currencies to revolutionize wholesale payments across borders.

A digital alternative to dollar-based settlement, critics say, could make it easier to evade sanctions, taxes and rules on money laundering, while fragmenting global payments into competing systems that further kindle geopolitical tensions.

Josh Lipsky, director of the Atlantic Council’s GeoEconomics Center, said it has “raised eyebrows” in Washington that mBridge is taking shape at the BIS.

“Taken in isolation it may seem strange because this project raises questions about China’s ambitions to reduce reliance on dollar-based settlement systems,” Lipsky said. “But China, like dozens of other central banks, is working with the BIS because this is where some of the most advanced research in the field is happening.”

Ross Leckow, deputy head of the BIS Innovation Hub that’s coordinating the project, said there’s no timeline yet for an operational system after the current stage of development. The next step, he said, is to see if the prototype can turn into a minimum viable product.

Read More: A Digital Dollar Is for Banks and Governments, But Not You

The Hong Kong Monetary Authority said there’s a shared goal of launching a minimum viable product next year, adding that the effort builds on the “G-20 priority to experiment with using new technologies to deliver cheaper and safer real-time cross-border payments and settlements.”

The Bank of Thailand praised the initiative’s goal of addressing “pain points” in cross-border transfers and said the BIS “continuously approaches additional jurisdictions to join the project.”

The People’s Bank of China didn’t respond to written questions about mBridge, nor did the Central Bank of the UAE offer a response.

mBridge is among at least six ongoing projects at central banks examining how digital currencies, also referred to as CBDCs, could be used to improve cross-border payments. Even as development plows ahead, their viability as a comprehensive alternative to the correspondent banking system that now links lenders around the world remains in doubt.

Even so, mBridge is considered so advanced that the International Monetary Fund hosted discussions in April on how to bring such a critical platform eventually under the control and supervision of an international organization, according to people familiar with the matter, who asked not to be identified discussing private information. The IMF wants to avoid having the project morph from technical solution to geopolitical tool, one of the people said.

In response to written questions, Federico Grinberg, a senior economist in the IMF’s monetary and capital markets department, said that it’s not planning on bringing any existing platform under international control or supervision, adding that the spring discussions were “technical” in nature and didn’t refer to mBridge specifically. “The IMF considers it essential that its wide membership is involved in this discussion given the disproportionate benefits of improving cross-border payments for emerging and lower-income countries,” he said.

The flow of digital money is a hot area of research because it can still be cumbersome to move funds over borders. Transfers require an orchestrated set of messages between private banks and central banks initiating and then confirming each step in the process. While many such transactions can settle within an hour, some can take days, especially if they involve smaller countries and currencies.

QuickTake: What Are CBDCs and Why Do Central Banks Want Them?

Because of the dollar’s liquidity and relatively stable value, companies around the world rely heavily on the greenback.

US Oversight

That affords the US significant economic and political advantages. Among other things, it means that an enormous proportion of cross-border financial flows must pass through banks licensed in the US that are subject to US regulation, its sanctions regime and tax system.

But moving dollars over borders is just as clunky, if not clunkier, as other transfers. Settlement typically happens during US working hours and can be held up by a holiday in any of the involved countries, providing an opening for a platform like mBridge — a name that refers to a multiple CBDC bridge.

The argument is that if the transactions happened on a digital rail enabled by blockchain technology, it could all be much easier.

The mBridge project report says trade financing is among the biggest planned uses, with about $564 billion worth of goods and services flowing among the participants.

It’s aimed at enabling large transfers and foreign-exchange deals directly between participating commercial banks after they have exchanged cash for tokenized currency at their central bank. And by using distributed ledger technology – similar to the foundation upon which Bitcoin operates – those transactions could happen almost instantly, any time or day of the week.

In August and September of last year, mBridge’s partners and commercial banks in their respective countries conducted a pilot trial facilitating about 160 transactions totaling $22 million in value, according to the latest project report.

Using the system, a company in China could pay a vendor in the UAE by having its bank issue a digital e-yuan token through the People’s Bank of China on the mBridge blockchain, or ledger. There, this token could then within mere seconds be credited to the vendor’s bank in the UAE, which would in turn credit the vendor’s account with dirham, the local currency.

According to two people with direct knowledge of the project, the technological backbone of mBridge is a Chinese-built blockchain.

Leckow disputed that assertion, saying the project is a collective effort and “several distributed ledgers were created with input from the four central banks” and the BIS. The application “would not be scalable by any one single party without participation from the others,” he added.

He also said “each participant commercial bank involved in testing on the mBridge platform is obliged to comply with applicable laws and regulations, including those related to tax compliance, money laundering and sanctions enforcement.” The project has a total of 23 international observers, including the US Federal Reserve and the European Central Bank, according to the BIS.

Days vs Seconds

If adopted and operational, mBridge would let commercial lenders in one country have access to a currency issued by another nation’s central bank instead of having to go through intermediaries or correspondent banks. While critics caution that it would give the parties a much better chance of dodging the dollar and circumventing sanctions or taxes, backers say the setup would remove significant friction.

Thailand’s central bank said mBridge can reduce cross-border transfer times from as many as five days to “several seconds,” according to an e-mailed response to questions from Bloomberg. It would also “offer more benefit to end-users and commercial banks if there are more participating jurisdictions to join.”

The US Treasury, which oversees sanctions compliance, the White House and the Federal Reserve, which directs monetary policy and oversees the country’s payments system, all declined to comment on the implications of the project.

Eswar Prasad, a professor at Cornell University and the author of “The Future of Money,” said the US government appears to be confident in the dollar’s preeminence and there’s little reason yet to be alarmed.

“Such initiatives could chip away marginally at the dollar’s dominance as an international payment currency,” he said. But, he added, it will leave China’s currency “well short of being in a position to seriously rival the dollar.”

The Atlantic Council’s Ananya Kumar, in an April post on China’s digital currency ambitions, also pointed to specific obstacles that could constrain mBridge’s impact, like the yuan’s liquidity.

It is unclear what will happen to mBridge once the development phase is finished. Technology built in past BIS Innovation Hub projects were used by participating central banks to build products of their own, for example the wholesale CBDC the Swiss National Bank plans to launch.

But there is no playbook for what happens if work from there becomes politically controversial.

The BIS confirmed that the global head of the Innovation Hub, Cecilia Skingsley, recently visited China, Hong Kong and Singapore for talks with the central banks involved in mBridge. The BIS’s Leckow said the hub’s core mandate is to test technologies, circulate the results and share lessons learned with the central banking community.

“We show what the technological possibilities are,” he said. “It is a matter for national authorities to decide whether to develop further or implement particular technological solutions.”

--With assistance from Eric Martin, Stephanie Davidson, Suttinee Yuvejwattana, Kiuyan Wong, Abeer Abu Omar, Yujing Liu and Chris Anstey.

Author: Bastian Benrath, Alessandro Speciale and Christopher Condon