There’s a growing need for the European Central Bank to rethink how soon it starts shrinking the €1.7 trillion ($1.8 trillion) stash of bonds it bought during the pandemic — or risk disorienting markets down the line.

At a meeting this week in Athens, the ECB is set to begin discussing ending reinvestments under the PEPP program before the current end-2024 cutoff. That would fully align quantitative-tightening efforts with interest-rate policy, which has delivered an unprecedented 10 straight hikes to drag inflation back toward 2%.

Some officials see PEPP purchases, which can currently act as a first defense should the bond yields of euro-zone governments jump unreasonably, as a key instrument amid budgetary jitters in countries like Italy.

But there are compelling grounds to halt reinvestments more quickly: Doing so too far into next year, or to match the existing deadline, risks the move happening alongside rate cuts to buoy Europe’s struggling economy, sending mixed signals to investors.

“We wouldn’t be surprised if the ECB brings forward the end to PEPP reinvestments by several quarters,” said Reinhard Cluse, chief economist for Europe at UBS. “What’s important is that they have to make an announcement before they start cutting interest rates. Otherwise, communication will be very difficult.”

With borrowing costs to be left on hold this week for the first time since the ECB began lifting them more than a year ago, officials are increasingly focusing on other parts of their toolkit.

Bonds from a larger portfolio — amassed from 2015 during fears of deflation — are already being allowed to roll off. But with the key policy rate at 4% to try to constrain economic activity and tame prices, PEPP reinvestments have become an outlier.

There’s a “strong argument in favor of stopping PEPP reinvestments sooner than the end of next year” because that would be “consistent with our interest-rate policy,” Governing Council member Madis Muller said last month.

The ECB hasn’t updated the program’s guidelines since December 2021 — well before rate hikes started. Back then, it promised future roll-offs “will be managed to avoid interference with the appropriate monetary stance.”

Barclays economists reckon an average of about €18 billion a month comes due under PEPP, though there are no official disclosures.

With the option to invest the proceeds of maturing securities across the currency bloc’s 20 members, some policymakers are wary to forgo such sums should debt markets take fright at the growing impact of the ECB’s hikes to date.

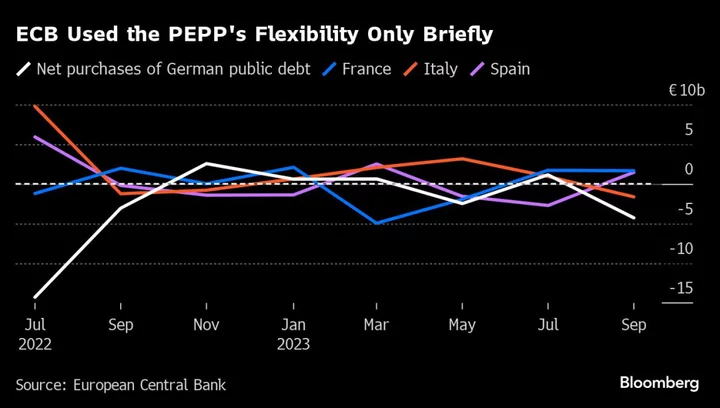

Flexibility was used immediately after it was introduced as officials tilted reinvestments toward Italy, Spain and Portugal and away from Germany and France.

While markets have since been steadier, the latest rout in Italian bonds is a reminder of how quickly investor confidence can fade. Even some ECB hawks, like Slovenia’s Bostjan Vasle, are hesitant to relinquish a tool that could restore calm if needed.

That’s especially the case as delays in overhauling European Union fiscal rules could prolong the lifespan of existing arrangements — potentially forcing governments into sharp fiscal consolidations and threatening penalties that could rattle investors.

But with Covid firmly in the rear-view mirror, leaving PEPP untouched is getting harder to justify.

“There are certainly some Governing Council members who’ll be concerned,” said Ulrike Kastens, an economist at German asset manager DWS. “On the other hand, bond reinvestments are expansive to a certain extent, so they don’t really fit into the landscape any longer.”

Comments from policymakers in recent weeks show the Governing Council is far from a consensus. A Bloomberg poll showed 43% of economists expect the ECB to bring forward the end to PEPP reinvestments — up from 39% before.

Kastens at DWS and her counterparts at Morgan Stanley are among those expecting a December announcement that reinvestments will start to be lowered as early as March, though a looming review of the ECB’s operational framework may mean more time is required.

Any concerns about breaking the pledge to maintain PEPP reinvestments through 2024 — a cost Dutch central-bank chief Klaas Knot said last month that he doesn’t think the ECB should incur “at this moment” — are likely to be overcome, according to UBS’s Cluse.

“The concept of forward guidance has been badly damaged over the past two years as a number of pledges by central banks were broken,” he said. “Compared with that damage, the additional credibility loss caused by shorter PEPP QT would in my view be quite limited.”

--With assistance from Harumi Ichikura.