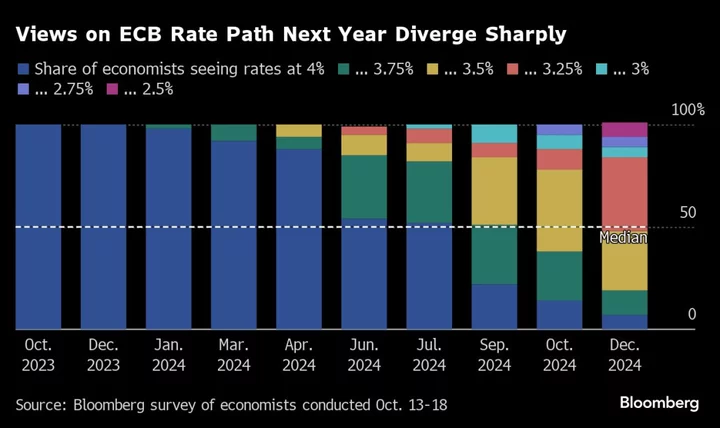

The European Central Bank will next week hammer home the message that borrowing costs are set to stay high for an extended period — despite risks to economic growth swirling, according to a Bloomberg poll of analysts.

Respondents don’t see any further interest-rate hikes and predict the Governing Council will confirm by January that a peak has been reached. They expect the first cut in September, following earlier moves to shrink the balance sheet more rapidly.

Having taken the deposit rate to a record 4% with 10 back-to-back increases, policymakers led by President Christine Lagarde have signaled they’ll hold fire to assess whether they’ve done enough to return inflation to 2%.

That stance has only been reinforced by the recent bond rout and the Israel-Hamas conflict, whose knock-on effects pose a further danger to 20-nation euro area’s already deteriorating prospects.

“Developments since the September meeting have worsened the euro-zone growth outlook but increased inflationary risks as oil prices surged,” said Carsten Brzeski, ING’s head of macro. “Against the background of higher bond yields and geopolitical tensions, a pause at next week’s meeting looks like a done deal.”

Following somber meetings of the International Monetary Fund in Marrakech this month, Lagarde told her global peers that the ECB can’t declare victory over inflation just yet, urging patience and caution in the face of potential new supply shocks.

Indeed, while price gains slowed markedly last month and wage pressures may be starting to abate, inflation expectations remain elevated. Meanwhile, a fledgling recovery for embattled manufacturers is being outweighed by wider economic threats.

What Bloomberg Economics Says...

“The weakness in the economy will probably prevent the ECB from increasing interest rates further. We look for the Governing Council to hold borrowing costs steady until June of next year, when it may reduce them.”

—David Powell, senior euro-area economist. Read more here

Just over 60% of survey respondents say downside risks to growth have increased since September’s ECB meeting, when staff trimmed projections through 2025. Nearly the same share said the balance of risks to prices has remained largely unchanged.

“Ebbing inflationary pressures accompanied by the broadening and deepening economic weakness suggests that ‘higher for longer’ won’t last very long,” said Nerijus Maciulis, chief economist at Swedbank. He predicts the first rate cut for April and sees the deposit rate falling back to 2% by March 2025.

Financial markets, too, are pricing a longer period of elevated rates. Yields on German two-year debt — among the most sensitive to changes in monetary policy — are about 3.2% and not far from their highest levels in 15 years. Money markets, meanwhile, are betting on a first quarter-point rate cut by July and another by the end of next year.

With interest rates on hold, policymakers are about to debate how to reduce the stack of bonds they bought under earlier stimulus drives more quickly.

Only about a third anticipates active sales from the ECB’s broader quantitative-easing portfolio — down from 43% before September’s meeting. But the share predicting an earlier end to reinvestments under the pandemic PEPP program rose to 43% from 39%. The majority sees roll-offs starting by the second quarter. The cutoff now is end-2024.

“If they announce a roll-off of the PEPP portfolio too early, Italian sovereign bond spreads could spiral out,” said Fabio Balboni, European economist at HSBC Bank. “But there are limited alternatives, with major changes to the reserves remuneration system seeming unlikely.”

While the latter topic has been broached by some officials as part of a wider look at how the ECB implements monetary policy, no adjustments are imminent.

The majority of survey respondents expects an increase in minimum reserve requirements within the next 12 months.

--With assistance from James Hirai.