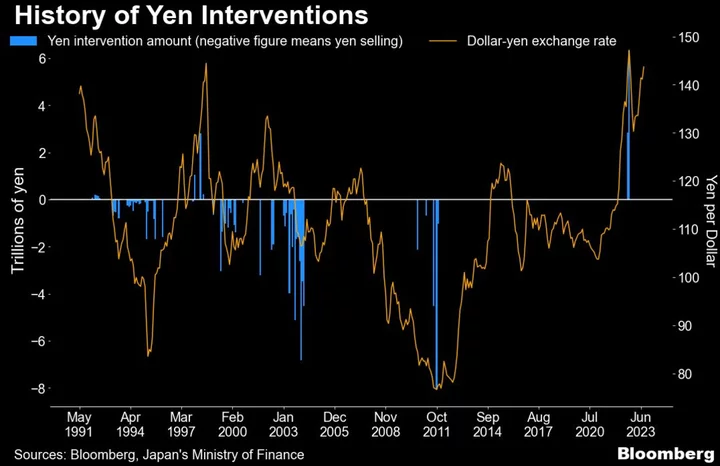

The yen remains vulnerable to sharp movements and government intervention even after its rally at the start of this week as key US data and central bank meetings loom large among potential catalysts.

US inflation figures on Wednesday are expected to show price growth accelerating for a second month in August versus a year earlier. If headline price growth outpaces the consensus for a 3.6% gain, reignited speculation of another US interest rate hike might boost the dollar, returning the yen to fresh year-to-date lows.

The pace of any yen slump will likely be the key to whether officials at Japan’s Ministry of Finance respond with ramped-up verbal warnings or consider action.

“But history suggests that levels matter to some degree, so there will be plenty of caution ahead of 150,” said Sean Callow, senior currency strategist at Westpac Banking Corp. “There may be some hints at looming action in terms of the frequency of public comments, but successful intervention usually requires an element of surprise, so the MOF doesn’t want to tip its hand.”

The current mood in the market, with the dollar hovering above 146 yen early Tuesday, is reminiscent of the situation a year ago, when the yen’s steep descent weakening prompted Japanese authorities to conduct the first yen-buying operations since 1998. While a weak yen supports exporters, it also raises the cost of food and energy imports, hurting households and creating a headache for Prime Minister Fumio Kishida.

Last year Japan needed to shell out more than $60 billion in three interventions before the tide turned in its favor and the dollar backed away from a multi-decade high of 151.95 yen in October. Convincing international allies of the need to step into markets again may be more difficult this year as interest rate differentials are even wider now than they were in 2022.

“The main argument against intervention any time soon is that the stark contrast between a dovish BOJ and US Fed funds rate at 5.38% justifies a weak yen. Most market participants probably regard the rise in USD/JPY since April as in line with fundamentals,” Callow said.

Unlike a year ago, a factor that may help Japan’s defense of the yen is the growing perception that the BOJ is moving closer to paring back its ultra-easy policy under a new governor.

Governor Kazuo Ueda said in an interview published Saturday that ending negative interest rates was among the options if inflation and wages keep rising. The BOJ may have enough information on both by the end of the year, he added. The comments bumped up support for the yen and boosted banking sector stocks on the hopes of higher interest rates.

But Ueda also said the bank remained some distance from achieving its price goal and that easing had to continue for now, comments that will put renewed downward pressure on the yen if they are repeated at next week’s policy meeting.

What Bloomberg Economics Says...

“The BOJ is sensitive to a weaker yen because it boosts cost-push inflation by lifting import prices — undermining prospects for demand-driven inflation it seeks. We think the BOJ is concerned about damaging second-round effects.”

— Taro Kimura, Economist

To read the full report, click here.

The BOJ’s next meeting ends on Sept. 22, while the Federal Reserve finishes its next two-day meeting on the 20th. Japan’s first intervention last year followed the Fed and BOJ meetings in September.

“I think the government has conveyed its frustration to the BOJ and wants the bank to do its part on dealing with the yen’s weakness,” said Mari Iwashita, chief market economist at Daiwa Securities Co. “I don’t think the government will intervene when its ammunition is limited.”

Meantime, finance ministry officials have kept up a drumbeat of verbal intervention. Finance Minister Shunichi Suzuki and top currency official Masato Kanda have increased their warnings, saying recently that the government won’t condone what it considers speculative moves in the market if they become excessive.

For now there have been no reports of currency officials contacting foreign exchange trading floors to ask what levels currencies are trading at. Such so-called rate checks effectively serve as a warning of possible imminent intervention.

Some currency forecasters and corporate officials are not seeing a break in the weakening trend anytime soon, with the 150-level considered a trigger level for potential intervention. As of the end of August, Japan had $1.25 trillion in foreign reserves it could use to prop up its currency.

Still, the macroeconomic context may erode appetite for such action, as Treasury yields may remain elevated, weighing on the Japanese currency, Ataru Okumura, a senior rates strategist at SMBC Nikko Securities Inc. in Tokyo, wrote in a research note on Monday.

“Yen intervention would prove to be futile and could even accelerate yen weakness,” Okumura wrote.

--With assistance from Masaki Kondo.