The surprising resilience of American consumers is about to be tested over the coming months, as rising delinquencies, growing debt payments and dwindling cash piles put pressure on household balance sheets.

Whether consumers pull back or power through is the biggest question facing Federal Reserve officials this week at their two-day policy meeting, where they’re set to hold interest rates steady in a range of 5.25% to 5.5%, a 22-year high. They’ll also debate whether another rate hike is needed at a future gathering, weighing the data on blockbuster growth that threatens to accelerate inflation, against expectations for a slowdown.

“If you look over the whole year things have been really solid and the question is, how much staying power does this have?” said Claudia Sahm, the founder of Sahm Consulting and former Fed economist.

The Fed’s aggressive campaign to tame inflation has made it more expensive for consumers to take out loans to buy homes or cars and made credit card debt more costly.

So far, it hasn’t dented overall demand. Americans spent broadly on furniture, travel and other splurges in the third quarter, government data showed last week, and the US economy expanded at the fastest clip in nearly two years. At the same time, the saving rate fell to 3.4% in September, the lowest this year.

Fed Chair Jerome Powell said that while forecasters expect growth to cool soon, officials are “attentive to recent data showing the resilience of economic growth” and will be watching consumer data carefully.

“Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy,” Powell said Oct. 19.

Budgets Squeezed

By some measures, consumers are struggling more to keep up with their bills.

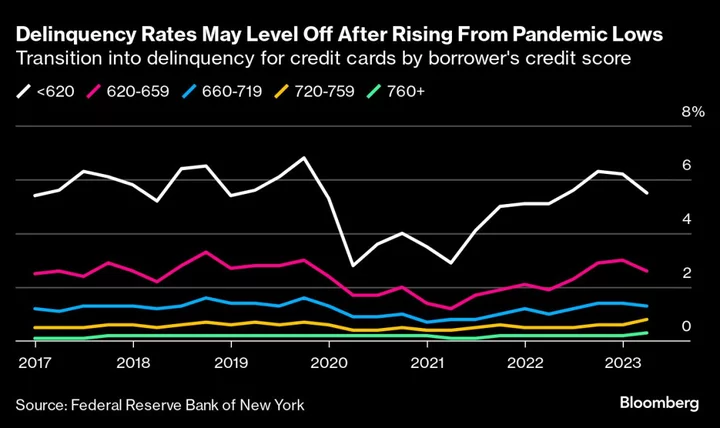

Delinquencies on consumer debt such as credit cards and auto loans are rising after falling to “unusually low” levels in 2020 and 2021 when consumers were benefiting from forbearance programs and federal aid, according to research from the New York Fed. They’re now back to the levels seen before the pandemic, raising questions about whether they will keep rising or stabilize.

After a temporary reprieve over the past three years, about 40 million consumers are also set to resume federal student loan payments this month.

The share of consumers who say they’re having a hard time with their expenses rose in October, according to the Census Household Pulse Survey. The increase was more pronounced for households with a college degree who earn between $50,000 and $150,000, “suggesting that restarting student loan payments is the source of increased financial stress,” Torsten Slok, chief economist at Apollo Global Management, wrote in an email note to clients.

US households spent 9.8% of their disposable income on debt payments in the second quarter, up from 8.3% in the first quarter of 2021 but still below the peak of 13.2% reached in 2007, according to Fed data.

The budget squeeze will likely continue, as income growth slows and rising rates plus the return of student loan bills push loan payments higher, said Anna Wong, chief US economist for Bloomberg Economics.

“Either you can sustain your spending habits of the past year or two by borrowing more, or you hold on tighter to your wallet or you go find more jobs,” Wong said

Potential Sweet Spot

Despite the looming headwinds, there are reasons to think consumers have enough momentum to keep the economy chugging along, economists say.

Job gains blew past expectations in September, helping to power spending last month. And recent data released by the Fed showed Americans experienced a record surge in net worth during the pandemic, laying the groundwork for resilience in 2023.

Many homeowners also locked in lower mortgage rates early in the pandemic, a move that reduced their monthly housing payments and left them with more disposable income. Some people also took advantage of the forbearance programs to pay down other debt, leaving them with a cushion of available credit they can tap into if needed, according to research released in October by the New York Fed.

“Right now, we’re kind of in the sweet spot and we could stay there,” said Sahm.

Also, the picture isn’t so dire once you consider that some people who changed jobs in recent years are earning higher incomes, and that delinquencies are rising from very low levels reached during the pandemic, said Jason Furman, an economics professor at Harvard University and former White House chief economist.

“There’s a question of whether there’s a slow easy adjustment for consumers,” he said, “or a Wile E. Coyote moment, whereas you sort of notice that your income is way below what your consumer spending is and you have to make some big adjustment.”

Alex Gras, a 27-year-old patent lawyer with $127,000 in student loans, faced his first student debt bill in October since graduating in 2021.

Gras, who lives in Dallas, expects he’ll be able to keep up with the monthly payments of about $800, but it means he’ll need to make smaller payments on the roughly $15,000 in credit card debt he accumulated from medical bills and living expenses while looking for a job after graduation.

“There are different areas I’m going to be cutting a little bit from,” said Gras, who expects to dine out less and is worried he may have to delay plans for buying a home. Still, he’s hopeful. “It will all work out in the end.”