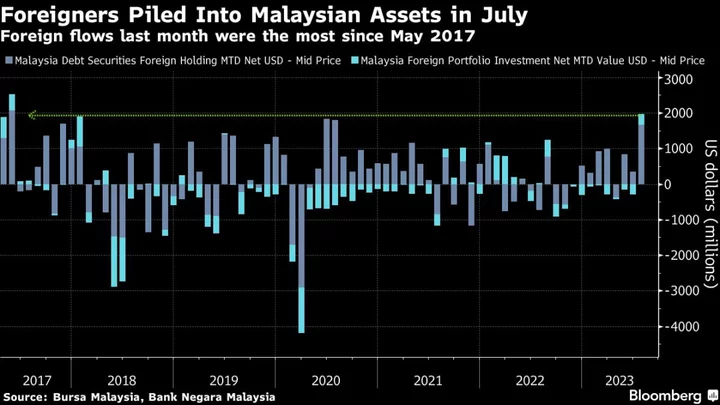

Foreign investors ramped up purchases of Malaysian assets last month in their hunt for carry returns amid bets global central banks are near the end of their tightening cycles.

They bought a total of about $2 billion of Malaysia’s stocks and bonds, according to data compiled by Bloomberg, the most since May 2017. More than 80% of the total inflows went into the nation’s corporate and sovereign debt.

Bond flows were likely concentrated in short-dated notes amid still attractive US dollar-hedged yields and a conducive environment for carry, said Winson Phoon, head of fixed-income research Maybank Securities Pte in Singapore. “Positioning at the short end with little duration risk, forex hedging and Federal Reserve rate nearing a peak has its appeal to churn carry and a better proposition from risk reward angle.”

The inflows come after a tough first half of the year as slow market-friendly reforms and sluggish demand from China dragged the nation’s stocks and currency to the bottom of the region’s performance rankings. The inflows have helped turn that around, with the ringgit now the best performer over the past month while stocks have climbed more than 5% over the same period.

“Investors are bottom fishing at this point,” said David Chao, global market strategist for Asia Pacific at Invesco Asset Management in Singapore. “Malaysian stocks remain cheaply valued and relatively defensive from external risks. Valuations for the KLCI are already at the lower-end of the range.”

Forecasts for Bank Negara Malaysia to leave its rate unchanged this year could help drive more inflows on expectations that returns on the nation’s debt will be maintained. This is in contrast to other emerging market economies such as Brazil, Chile and Hungary which have begun cutting rates.

Foreign investors net purchased about $31 million worth of Malaysian stocks this month as of Aug. 9, according to Bloomberg compiled data after purchasing $313 million of stocks in July.

Short-Lived Boost

Still, the strong inflow into Malaysia may not last amid risks of China’s economic woes spilling over into the region and renewed strength in the dollar.

“A slower-than-anticipated economic recovery in China alongside a prolonged period of restrictive monetary policy across developed markets in particular suggest a more challenging global growth prospects for 2H23 and beyond, implying more cautious risk sentiment ahead,” Loke Siew Ting, an economist at United Overseas Bank Ltd. wrote in a note to clients.

--With assistance from Marcus Wong.