US stocks are back in a bull market and the American economy has consistently outperformed expectations, leading some firms to suggest the threat of recession has eased, if not altogether passed.

Such thinking, though, risks a grave error for investors, according to some of the world’s biggest bond managers from Fidelity International to Allianz Global Investors. They’re sticking to their forecasts for a downturn and advise hedging any bets on risk assets.

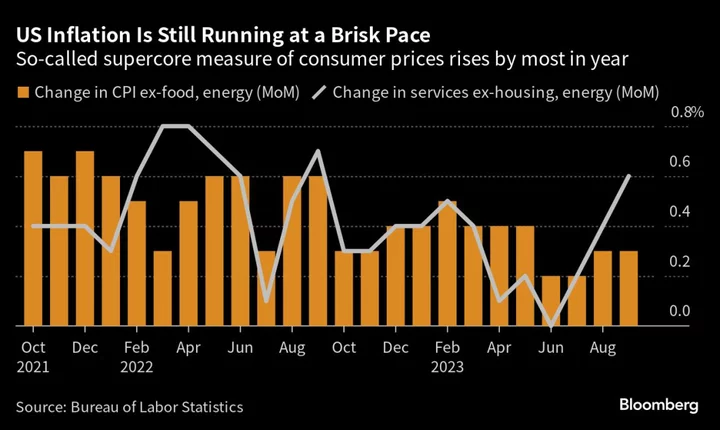

By their reckoning, the damage from 10 straight increases has been done and the collapse of three US lenders in March was just a taste of the bigger crisis to come as central banks stay hawkish until something else breaks. Just last week, Canada and Australia delivered surprise hikes, putting some pressure on the Federal Reserve to follow at an upcoming meeting as inflation remains persistently high.

“Something akin to a credit crunch is what I’m most concerned about,” said Steve Ellis, global fixed-income chief investment officer at Fidelity International, which manages $663 billion of assets. Central banks’ continued tightening shows they’re “fighting last year’s battle,” he said.

Ellis has built up duration risk, market parlance for interest-rate sensitive assets such as government bonds, on the grounds that when central banks are forced to switch to a pause or to looser policy, they will outperform. He sees the 10-year Treasury yield falling to 3% by year-end, nearly 75 basis points below the current level, as markets start to realize the recession will be deeper than most think.

At the same time, junk-rated corporate bonds look vulnerable to a correction, Ellis said. Fidelity’s analysis suggests the sector is pricing in a corporate default rate of about 4.6%, when in reality it will be closer to 8%.

For Mike Riddell, a portfolio manager at Allianz Global Investors, stocks, bonds and corporate debt are mispricing the risks, and only inflation-rate swaps have the economic outlook right. The so-called one year, one year forward inflation rate is currently at 2.4%, or close to 2% when risk compensation for investors is factored out. That implies a “nasty recession” within the next six months, he said.

“Our base case is for a moderate-to-deep recession — and potentially crises — as the unprecedented pace of global policy tightening seen over the last year starts to really bite,” Riddell said. He recommends being bullishly positioned in rates and bearishly positioned in risk assets like credit.

Money market traders are wagering on a 90% chance of another quarter-point hike from the Fed by July. Investors are also expecting at least another 50 basis points of hikes from the European Central Bank — starting at next week’s meeting. That’s despite the bloc already brushing with recession in the first quarter and growing issues in Germany, the region’s economic powerhouse.

To be sure, the recession is taking far longer to show up than many envisaged at the start of the year, and it’s possible the economy may keep defying expectations. Nonfarm payrolls, which surged in May, surpassed all estimates.

The resolution of the US debt ceiling saga also helped improve sentiment and was cited by Goldman’s economists in lowering the odds of a US recession in the next 12 months to 25%. Goldman Sachs Group Inc.’s Chief Operating Officer John Waldron, says a recession may not happen.

But signs of consumer pain are mounting.

Credit-card balances, which hit $986 billion in the fourth quarter of last year, remained largely unchanged in the first quarter for the first time in more than twenty years. Normally they post a dip as people pay off their debts from the holiday season.

“Consumers are stretched, so I’m not 100% sure that a soft landing is really realistic at this point,” said Patrick McDonough, a portfolio manager at PGIM. “The downside is becoming more and more likely, just because we’ve been propped up by consumers for so long.”