China should ramp up government borrowing, offer more tax breaks to businesses and keep cutting interest rates to revive the economy and stem rising unemployment.

That’s according to several government-linked economists and a respected former policymaker, who all see an increasing urgency for Beijing to take decisive action to respond to the slowing rebound with additional stimulus.

The world’s second-largest economy is flashing warning signs: The property market is sputtering, infrastructure investment is flatlining and exports are shrinking. The youth jobless rate is at a record high and deflation risks are looming — all problems weighing on business and household confidence.

Here’s a look at some options the government has to try to get the recovery back on track:

Borrowing More

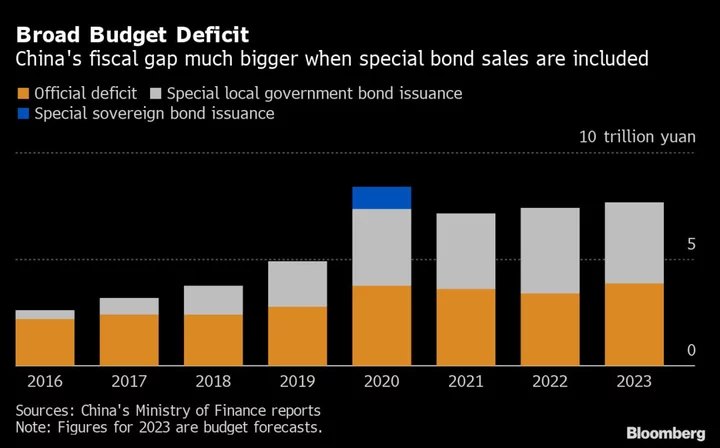

The government could raise its budget deficit, which was set at 3.88 trillion yuan ($541 billion) in March, excluding the amount of new special bonds regions are allowed to sell this year. Authorities may be wary of doing so given the long-term risks associated with rapidly building up debt, like what happened after 2008.

But short-term fiscal expansion could still help the economy, and moving fast would keep costs relatively low, according to former finance minister Lou Jiwei.

“The budget deficit should be raised in a timely manner to restore the economy to its normal state as soon as possible,” Lou wrote in an article carried Sunday on the front page of the Economic Daily, a newspaper affiliated with the State Council, China’s cabinet.

Lou called on the government to raise this year’s fiscal deficit by up to 2 trillion yuan, which would boost the deficit-to-GDP ratio to as high as 4.6%, according to Bloomberg calculations based on official data. Beijing’s target is 3%.

“The price paid will be the minimum and fiscal sustainability won’t be undermined,” Lou wrote.

The government is also weighing plans to allow the issuance of additional local bonds to help cash-strapped, high-risk areas pay down their hidden debts, people familiar with the matter told Bloomberg News earlier this month.

Sovereign Bonds

Any new debt should be mostly sold by the central government and used to help small businesses, Lou said. Some of the money could also go to strained local governments to stop them from going overboard on measures to find income, such as imposing excessive fines on people, he said.

Liu Shangxi, head of the Chinese Academy of Fiscal Sciences — a think tank associated with the Ministry of Finance — suggested the central government still has room to add leverage compared with local authorities.

In an interview with the government-run China Newsweek, he argued the central bank should cast aside a “dogmatic” insistence about being independent, and start buying central government bonds directly to spur growth.

“The function of monetary policy alone is limited when the economy is in a down cycle, and it should act as a complement to the implementation of fiscal policy, rather than independently,” Liu said.

The People’s Bank of China has long resisted calls to buy bonds directly from the government because of concerns about monetizing the deficit or oversupplying the economy with money, thus causing inflation to spike out of control.

Instead, the PBOC has mainly used notes as collateral for lending to commercial banks.

Rate Cuts

The central bank could also ease any burden the government shoulders from taking on new debt by continuing to cut interest rates to keep financing costs low. Injecting more liquidity into the banking system would also help absorb the issuance of debt.

The PBOC is likely to shave policy interest rates moderately through the rest of 2023, according to economists surveyed by Bloomberg. But some Chinese policy advisers and government-affiliated economists have recently floated larger cuts.

Reducing interest rates by 100 basis points would save 3.1 trillion yuan worth of financing costs across the country — more money than industrial firms made in profit for the first five months of the year, according to economist Liu Yuanchun, who has in the past consulted with top leaders including President Xi Jinping.

Former PBOC Yu Yongding said earlier this month lower interest rates were “very necessary” and the room for cutting was “relatively big.”

Reserve Ratio

Far more likely than a massive policy rate cut: Additional trims to the reserve requirement ratio, or the amount of cash banks must keep in reserve.

The PBOC last reduced that ratio in March. But it may be compelled to do so again in the second half of 2023 to avoid a cash crunch when a bunch of policy loans comes due.

The central bank could also encourage banks to extend more loans, given the weakness of overall credit expansion. New PBOC Communist Party Chief Pan Gongsheng — who is widely tipped to become governor — suggested last month there is room for credit growth to pick up.

At the end of June, the PBOC also increased the quota for relending and rediscounting programs that support the agricultural sector along with small and private firms. The central bank may be looking at more ways to funnel bank loans into targeted sectors via structural tools, according to the Shanghai Securities News.

Tax Incentives

Former Premier Li Keqiang oversaw the rollout of tax cuts to help companies weather the impact of the US-China trade war and the pandemic. Those measures were massive in scope: Tax income last year was nearly 14% of GDP, compared to 17% in 2018.

The room for further aggressive cuts is probably slim, given how much government income has contracted during the property market downturn and as land sales, a key source of income, slump.

Instead, the government should focus on improving the effectiveness of existing tax breaks, wrote Yuekai Securities Co. Chief Economist Luo Zhiheng in an article published in China Finance magazine, which is affiliated with the PBOC.

Luo also attended a meeting held last week by Premier Li Qiang, where Li told several prominent economists the government would “spare no time” in implementing targeted stimulus.

More tax incentives may be on the way. The government is considering measures worth hundreds of billions of yuan targeted toward high-end manufacturing companies, Bloomberg News reported in May. Some analysts also expect similar favorable measures for integrated circuit board makers to help with research and development.

Cash Subsidies

Luo also suggested the government provide consumption coupons or cash subsidies to encourage household spending. Costs could be shared between the central government and local ones, with poor regions responsible for a lighter burden, he wrote in the China Finance article.

That may be a long shot: During the pandemic, Beijing refrained from giving consumers direct cash handouts on a large scale, as the US and other countries did. Instead, the government bet that a recovery in hiring would lead households to spend more. But dour confidence has yet to abate and limited stimulus measures have done little to reverse course.

Luo also floated some longer-term solutions that have made the rounds in recent years, including a reform of the nation’s income distribution system.

He wrote that farmers should receive stronger social security protections, while migrant workers should get broader access to urban public services so they are able to spend more. Liu of the finance ministry think tank has echoed similar proposals.