Perpetual dollar bonds sold by several Hong Kong-based companies have recently suffered their largest weekly declines in years, a sign of contagion from China’s property sector woes.

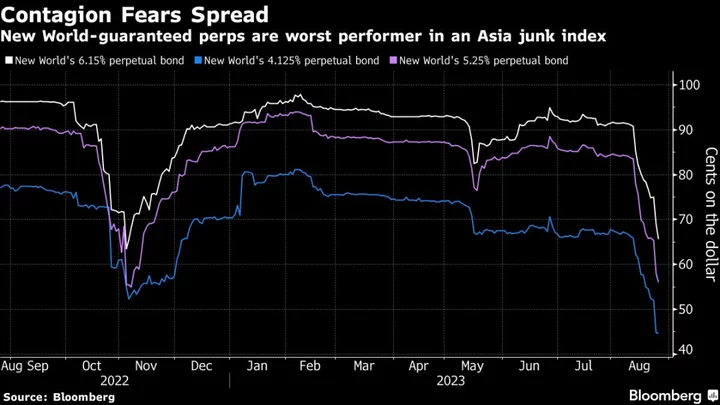

Notes guaranteed by New World Development Co. — one of Hong Kong’s most indebted real estate firms — have tumbled about 10 cents this week, extending last week’s record losses of as much as 17 cents, according to prices compiled by Bloomberg. One bond is at a record low of 44.6 cents while others are near last year’s bottom. Perpetuals backed by New World have lost 15% this week, the worst performer in a Bloomberg index of Asia high-yield dollar notes.

Price declines in other Hong Kong firms’ perpetual bonds have accelerated in recent days. Notes from fellow builder Hysan Development Co. and supply chain firm Li & Fung Ltd. have fallen at least 5 cents this week, putting both on pace for their largest such drops since March 2020.

“The offshore bond market contagion is spreading to the Hong Kong high-yield and non-rated bond market given their direct and indirect onshore property exposures,” said Owen Gallimore, head of Asia-Pacific credit analysis at Deutsche Bank AG. “The selloff is most keenly felt in the perpetuals given the smaller investor base for this product and subordination.”

Perpetual notes are issued without a maturity date or have very long tenors such as 50 years. They are often more volatile due to their sensitivity to interest-rate changes. The bonds are a type of subordinated or junior subordinated debt, meaning higher risk that investors are wiped out in case of a default.

China’s property woes haven’t caused direct impact to Hong Kong’s major developers. But builders are facing higher borrowing costs amid interest rate hikes, and sales for new residential units are at a 4-year low. Hong Kong’s once-hot office market is also going through its worst downturn in years.

New World is the property-development arm of Hong Kong’s billionaire Cheng family, which is building the city’s largest shopping mall. The company earlier this year laid out a deleveraging road map, months after Chief Executive Officer Adrian Cheng said in an interview that it was “a good opportunity to start acquiring our war chest” in China. New World shares fell as much as 7.2% Friday to their lowest level since Nov. 4.

The country’s real estate sector is undergoing fresh liquidity pressure, highlighted by the debt-repayment difficulties at China’s former largest builder. New-home sales and prices have been falling while the national economy has slowed.

Recent perpetual-note declines also include Hong Kong-based Bank of East Asia Ltd., a lender with a comparatively high rate of soured loans to China’s real estate sector and last year underwent a bond rout. One of its perpetuals is down 10 cents this month, set for the most this year.

Nonperforming loans in BEA’s China property book remained around 20% even after charging off some borrowings in the first half of this year, according to Bloomberg Intelligence credit analysts Pri de Silva and Adrian Sim. “This could potentially signal shaky credit quality at some Chinese banks,” they wrote this week.

--With assistance from Alice Huang and Pearl Liu.