Sign up for the India Edition newsletter by Menaka Doshi – an insider's guide to the emerging economic powerhouse, and the billionaires and businesses behind its rise, delivered weekly.

India’s inflation slowed sharply, while manufacturing production surged more than forecast, giving the central bank reason to keep interest rates unchanged for longer as it assesses the outlook for the economy.

The consumer price index rose 5.02% in September from a year earlier, the slowest pace in three months and below economists’ forecasts, largely due to lower food prices. Growth in factory output surged to a 14-month high of 10.3% in August, government data showed Thursday.

While inflation is now well within the Reserve Bank of India’s 2%-6% target range, Governor Shaktikanta Das last week emphasized that the central bank is targeting the 4% midpoint, signaling monetary policy would remain relatively tight for some time. The jump in manufacturing may also give the RBI reason to be cautious as stronger demand drives up prices and worries over oil prices and poor weather conditions remain.

The 4% target “is unlikely to be achieved soon,” Alexandra Hermann, an economist at Oxford Economics, wrote in a note. “The impact of below average monsoon will keep prices for certain food items such as cereals and pulses elevated for longer while oil prices are likely to rise in the fourth quarter. We therefore don’t believe a rate cut is in the cards before the second quarter of 2024.”

Das said Thursday the September print was “exactly in line with our internal projections” and policymakers realized the recent rise in inflation, led by vegetables prices was a “temporary spike” that would moderate after two months.

“So, we did not do a new knee-jerk reaction of doing something on the rate side,” Das said during a discussion at International Monetary Fund’s annual meetings at Marrakesh. Active coordination between the fiscal and monetary authorities are helping the central bank keep a lid on prices, he said, with the RBI keeping rates elevated and the government taking measures to lower vegetable prices.

What Bloomberg Economics Says

A sharper-than-expected slump in India’s inflation in September is likely to soften the central bank’s stance on keeping liquidity conditions tight. Even so, we think the central bank is likely to keep rates on hold a bit longer until there’s clarity about future Federal Reserve policy.

Abhishek Gupta, Senior India economist

For the full report, click here

Food prices, which make up about half of the inflation basket, rose 6.56% in September from a year ago, down from 9.94% in August. Fuel and electricity costs fell 0.11% while growth in housing prices accelerated to 3.95%. Core inflation, which strips out volatile food and energy prices, eased slightly to 4.57%.

Inflation is a worry for Prime Minister Narendra Modi’s Bharatiya Janata Party, which faces crucial state polls next month and national elections in summer of 2024.

The government has taken a number of steps in recent months to curb prices pressures. It’s imported tomatoes and imposed curbs on exports of rice, wheat and sugar to tame food prices ahead of the festive season that will peak in November. Cooking gas prices have also been slashed.

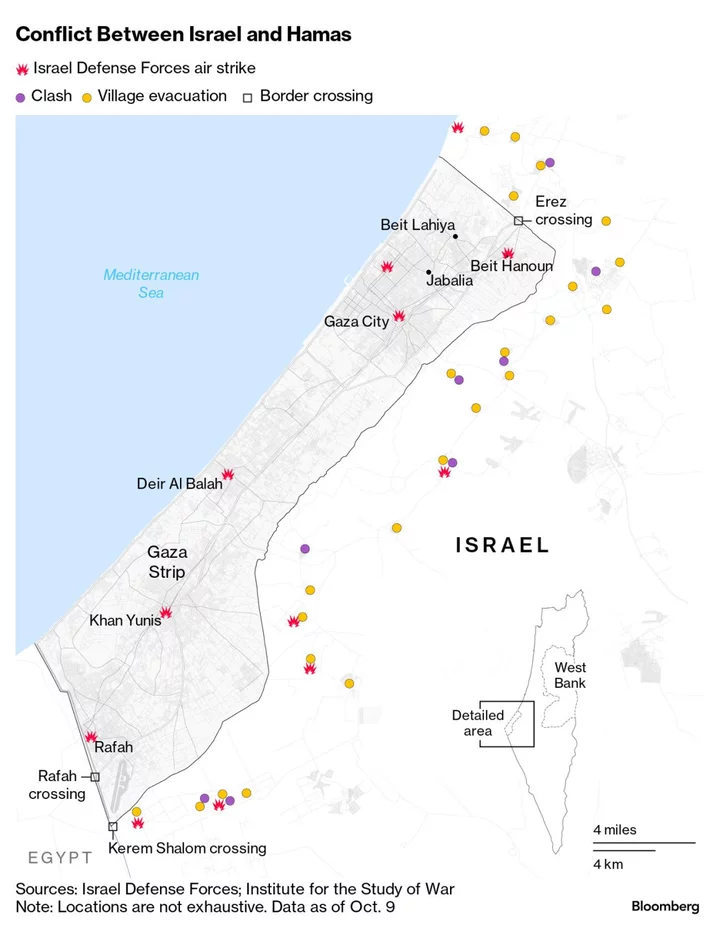

Rising international crude prices remain a key threat to India, the world’s third-largest consumer of oil, most of which is imported. The conflict between Israel and Hamas has increased uncertainty about the outlook for prices as well as prospects for the global economy.

“Higher crude oil prices and persistence of price pressures on cereals and pulses remains to be watched,” said Upasna Bhardwaj, an economist at Kotak Mahindra Bank.

(Updates with comments from RBI Governor, economists.)