By Jamie McGeever

A look at the day ahead in Asian markets from Jamie McGeever, financial markets columnist.

The word 'crisis' should always be used responsibly and judiciously when covering financial markets, business and economics, but are we at that point now with China?

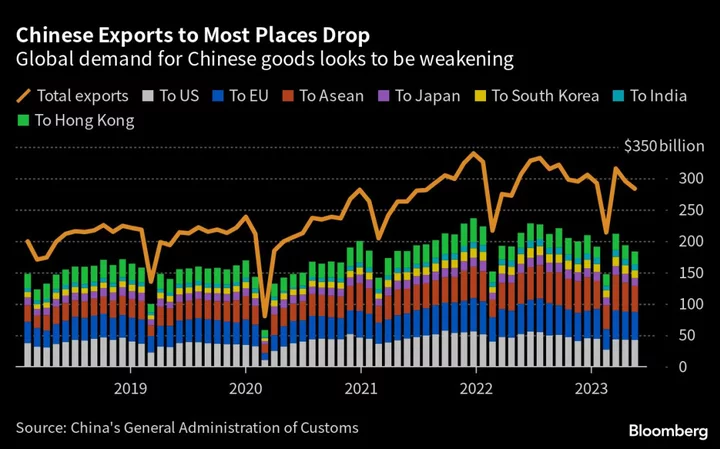

Developments in the last 24 hours from the world's second largest economy - another string of top-tier data 'misses', a shock interest rate cut and an abrupt announcement that (record high) youth unemployment data will no longer be published - suggest we might be.

The deepening concern around China's economy, policy options and financial markets will weigh heavily on Asian investor sentiment on Wednesday, with an interest rate decision from New Zealand and the latest manufacturing and service sector 'tankan' surveys from Japan also on tap.

It's not all doom and gloom in Asia - Japan's economy grew twice as fast in the second quarter as economists had expected - but China's travails are front and center right now.

Perhaps even more worrying for investors than the misses on investment, industrial production and retail sales, or the surprise rate cut, was Beijing's decision to suspend the publication of youth unemployment figures for an unspecified length of time.

The official rate in June was a record 21.3%. That's bad enough, but in an online post last month - since removed - Peking University professor Zhang Dandan estimated it could be closer to 50%.

The latest snapshot of Chinese house prices will be released on Wednesday, and again, another weak report could be in store, with the country's property sector in a genuine state of crisis.

JP Morgan on Tuesday said if developer Country Garden suffers a full-scale default, it will more than double China's year-to-date property default tally to $17 billion, adding to the $100 billion racked up over the past two and a half years.

The People's Bank of China may have finally pulled the interest rate lever, but it had the expected impact of slamming the exchange rate. The offshore yuan tumbled through 7.30 per dollar to its weakest level this year and is now flirting with November's historic low of around 7.35 per dollar.

Compare and contrast China with Japan, as per Tuesday's bumper Q2 GDP data, and the U.S., where figures on Tuesday showed a surge in retail sales. The Atlanta Fed's GDPNow model is projecting annualized Q3 growth of 5.0%.

Global stocks, Wall Street and emerging markets all buckled on Tuesday under the weight of rising bond yields, 'higher for longer' Fed rate expectations and a buoyant dollar.

The MSCI Asia ex-Japan index fell for a fourth day and has now only risen twice in the last 11 sessions. Among the biggest losers in Asia on Tuesday was Hong Kong's mainland property index, which fell 1% to take its year-to-date decline to 16%.

Here are key developments that could provide more direction to markets on Wednesday:

- New Zealand interest rate decision

- China house prices (July)

- Japan tankan surveys (August)

(By Jamie McGeever; Editing by Josie Kao)