When it comes to the bond market, it’s Morgan Stanley vs Bill Dudley now.

In their latest assessment of the bond market outlook, Morgan Stanley strategists are challenging the former head of the Federal Reserve Bank of New York’s view that losses are likely to deepen.

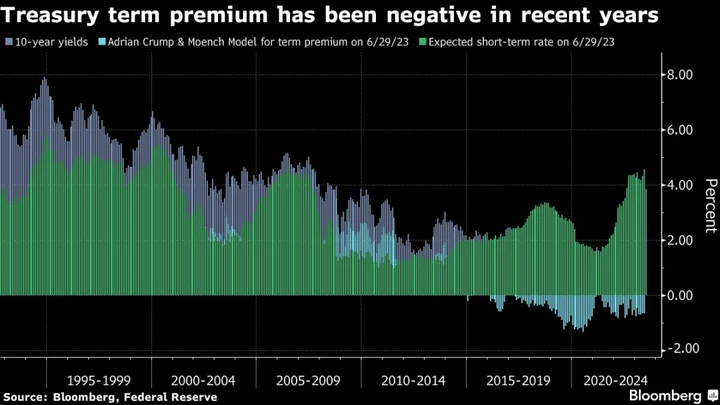

Dudley’s estimates of key drivers for the 10-year Treasury yields — including the real federal funds rate, inflation and term premium — are too high, strategists led by Matthew Hornbach say in a June 30 report. Instead of heading for 4.5% as Dudley predicted last week, the 10-year Treasury yield, currently about 3.85%, is likely on course for a range of 2% to 3%, they say.

“While some describe the bond market sell-off as ‘far from over,’ we disagree and call it ‘long in the tooth,’” the Morgan Stanley strategists wrote. Dudley didn’t immediately respond to a request for comment on Morgan Stanley’s broadside.

Dudley, who led the New York Fed from 2009 to 2018 after spending nearly 20 years at Goldman Sachs, ultimately as chief US economist, predicted in a June 29 Bloomberg Opinion column that 10-year yields are likely to rise to a level last seen in 2007. Because people are unaccustomed to such high borrowing costs, “further havoc is all but guaranteed,” he wrote.

In their rebuttal, the Morgan Stanley strategists said Dudley’s assessment that the real federal funds rate will average 1% has “a very low probability” of coming to pass. The rate “barely reached 1.0% in 2019 and has not yet eclipsed 1.0% in the current hiking cycle,” they wrote. “A more reasonable estimate” is 0% to 0.5%.

Where Dudley predicts 2.5% average inflation over the next decade, Morgan Stanley looks for 2%, a quarter-point higher than average for the decade before the pandemic.

As for term premium, which Dudley says should be 1%, Morgan Stanley says the expansion of central bank balance sheets leave “very little scope for term premiums to rise.” Elevated policy rates also will help contain the average term premium between 0% and 0.5%, the strategists say.

Treasury yields have scope to decline beginning in mid-July, Guneet Dhingra, Morgan Stanley’s head of US interest rate strategy, said in the report. Seasonality turns favorable at that time, and the market may get additional support from reserves stabilizing, June inflation readings and bank earnings reports for the first full quarter since several institutions failed in March.