Oil fell after a breakneck rally as wider markets held a cautious tone ahead of a Federal Reserve meeting, and crude’s metrics continued to signal that prices may have risen too far, too fast.

West Texas Intermediate for November dropped toward $90 a barrel, after closing almost level on Tuesday. Its 14-day relative strength index has been above 70 since the start of this month, suggesting a pullback may be imminent. The October contract for the US crude benchmark expires later on Wednesday.

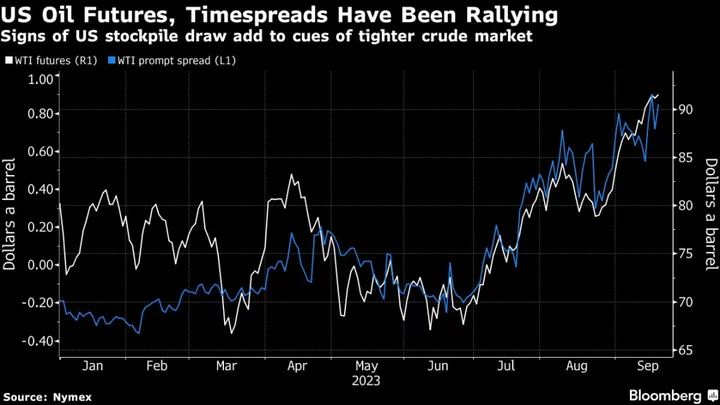

Crude has roared higher this quarter, hitting a 10-month high, thanks to supply curbs from OPEC+ linchpins Saudi Arabia and Russia, as well as brighter outlooks in the two biggest economies, the US and China. While the upswing has reignited talk of a return to $100 oil, that may be a headache for central bankers, including those at the Fed who decide policy later Wednesday.

Oil is “taking a breather with FOMC event risk ahead,” said Charu Chanana, market strategist at Saxo Capital Markets Pte in Singapore, referring to the rate-setting Federal Open Market Committee. Still, “$100 oil chatter remains,” she added, citing tightness in physical markets, including diesel.

Widely tracked measures of supply and demand reinforce signals that the market is tightening. In the US, the industry-funded American Petroleum Institute said that nationwide inventories shrank by 5.25 million barrels last week, including a drawdown at the Cushing hub, according to people familiar with the figures. A separate assessment from AlphaBBL Corp. also showed a drop at the Oklahoma storage site. Official data come later on Wednesday.

In addition, timespreads retain a strong tone. The gap between WTI’s two nearest December contracts held just below $10 a barrel in a bullish backwardated structure, more than twice the figure a month ago.

To get Bloomberg’s Energy Daily newsletter into your inbox, click here.