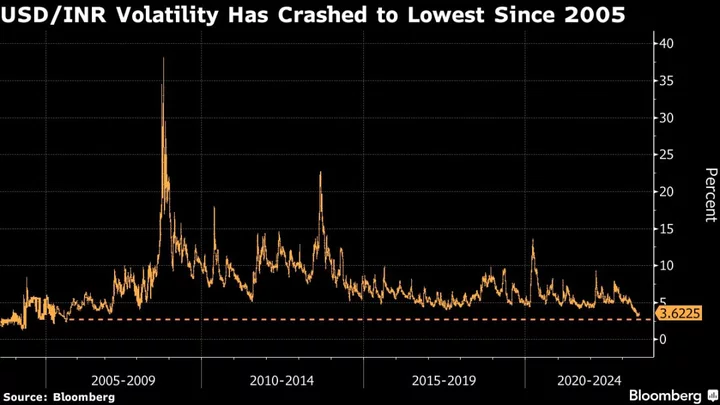

Even in a year where currency volatility is falling worldwide, the slump in swings in the Indian rupee has traders from London to Singapore asking when the central bank will loosen its iron grip.

The rupee’s one-month implied volatility versus the dollar crashed to its lowest since 2005 in June, drawing queries from investors on roadshows of Citigroup Inc. and ICICI Securities Primary Dealership Ltd. to gauge the path ahead for the Indian currency. That’s largely because of the outsized role of the Reserve Bank of India in keeping the rupee in a tight range.

The RBI has added back $32 billion in reserves already this year as it absorbed foreign inflows to keep the currency steady, while its dollar forward book also climbed by around $10 billion in the first four months of the year. The central bank’s efforts for a stable rupee may be aimed at boosting its appeal as an international trade currency, according to Citigroup.

“Fixed-income investors are basically looking for ways to trade the Goldilocks environment in India and the clearest way for those that believe dollar can weaken also is to go long the rupee,” said Abhishek Upadhyay, economist at ICICI Securities Primary Dealership, who is back from a recent client trip to Singapore and Kuala Lumpur. “Traders clearly want higher vols, even as investors are still willing to wait longer for RBI to let go of rupee.”

The rupee’s historical volatility is the lowest in Asia over the past year, barring the pegged Hong Kong dollar. It has coincided with a global decline in assets volatility. The JPMorgan Global FX Volatility Index is at 8.2%, down from this year’s high of 11.6% seen in March.

The rupee’s gains have been muted this year despite over $12 billion of inflows into the nation’s stocks, while its high-yielding rival Indonesia is up about 3% with only a small fraction of those inflows. RBI has maintained that it intervenes to keep undue rupee volatility in check.

Investors from M&G Investments Inc. to T. Rowe Price Group Inc. are largely positive on the rupee driven by improved macros and the world’s fastest-growing major economy.

“India’s balance of payment has moved back into surplus,” said Guan Yi Low, head of fixed income, Asia Pacific at M&G. “India is also benefiting from the relocation of global supply chains. We see upward potential for India’s growth outlook in the coming years, and are positive for the rupee.”

The rupee stability has analysts and investors discussing the RBI’s currency strategy, and its pros and cons.

“RBI may be ascribing the same weight to currency stability as it does to price stability and financial stability in an uncertain global environment,” Samiran Chakraborty, India economist at Citigroup, wrote in a note.

Yet, the dangers of lower volatility can’t be overstated. Historically, long periods of unusual stability in the rupee have been followed by a sharp depreciation as periods of tranquility can lead to complacency, according to Citigroup.

“The negative side effects of low volatility are often insufficient hedging by corporates which can lead to unwanted currency exposure in case of a sharp downward move in the rupee,” said Rajeev De Mello, global macro portfolio manager at Gama Asset Management in Geneva. “Foreign investors adjust their positions based on volatility and could increase their rupee positions excessively.”