All the chatter back in December was that 2023 was to be the “year of the bond.” And for a brief moment or two in the winter, that call — and the economic doom-and-gloom that underpinned it — looked right.

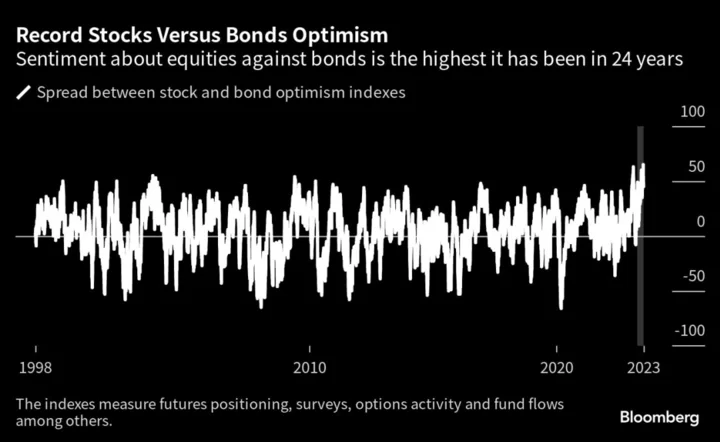

It is now being overrun, though, by an avalanche of demand for equities that has unleashed a furious rally across the globe and, in a sign the gains are likely far from over, made investors more optimistic about stocks relative to bonds than at any point since SentimenTrader models began comparing them 24 years ago.

“As sentiment, technicals and risk of the recession got pushed further out we moved from being underweight stocks to overweight,” said Nathan Thooft, global head of asset allocation at Manulife Asset Management in Boston, who’s reduced his credit exposure in favor of an equity overweight.

2023 had all the makings of a breakout year for fixed income. The end of aggressive Federal Reserve rate hikes and a pivot to easier policy should have set up a rally in bonds and made them an insurance policy against a growth downturn.

Instead, the economy seems to have pulled off a rare feat: inflation has slowed while new jobs are being created. Growth keeps accelerating and even staff at the US central bank are no longer forecasting a recession. The Fed is still raising rates — though it may have just completed its last increase this week — and bonds aren’t living up their billing as a safety valve.

The surprising reversal has found some prominent sell-side strategists issuing mea culpas, others upgrading their stock targets, and more downgrading their recession forecasts or giving them up altogether.

More than half of clients surveyed last week by JPMorgan Chase & Co. say they are now convinced the US economy can continue to expand despite rapid-fire hikes, so-called “soft” or “no landing” scenarios. The survey shows a jump in the number of investors planning to boost equity exposure at the expense of bonds.

That’s already happening. Discretionary investors — who allocate cash based on their view of the economy — have ramped up their pace of stocks buying on par with the time of the vaccine announcement in late 2020, according to Deutsche Bank AG. Flows into exchange-traded funds show a strong preference for equities over fixed income in the last three months, a big reversal from the start of the year.

“The bears were loud all year and still are and meanwhile the market climbed the wall of worry perfectly the entire time,” said Ken Mahoney, chief executive officer of Mahoney Asset Management. “We definitely can understand their point of view. But they are missing out on the technicals that have been telling us stocks are working their way higher.”

It’s not like predictions that bonds would win this year have been entirely wrong — across the curve they’ve posted positive returns and investors are collecting big yields for little risk. It’s just that equities have posted once-unimaginable gains this year — the tech-heavy Nasdaq 100 is up 44% — that’s juiced their relative performance in ways that have blindsided Wall Street pros.

And while the soft-landing scenario is now the market’s favorite, it’s by no means certain.

“What the market’s now pricing is a soft landing — a lot has to go right for that, and the risks are in one direction,” Alex Brazier, deputy head of BlackRock Investment Institute, said in an interview with Bloomberg TV.

The lagged effect of 525 basis points of Fed rate hikes could take two years or more to ripple through the economy. The disinflation trend might be a blip that owes too much to falling oil prices. Tech stocks in the S&P 500 trading at 28 times prospective earnings may mean they are ripe for a selloff while positioning is so skewed to the upside, any pullback risks a bigger fall.

Still, Brazier admitted this year so far isn’t turning out like he and his BlackRock colleagues anticipated.

“What’s happened, particularly in the US stock market, has taken a lot of people by surprise,” he said.

SentimenTrader suggests the shift may endure. Unlike in the past, corporate insiders are big buyers, while technicals like subdued volatility and bullish options are keeping equity sentiment elevated.

The only other two instances when stocks versus bond sentiment were so wide apart were in 2003 and 2009 “both coming out of protracted bear markets and indicating a dramatic shift in investor expectations,” said Jason Goepfert, director of research at Sundial Capital Research and SentimenTrader, which analyzes futures positioning, surveys, options activity and fund flows. “Both preceded new bull markets.”

--With assistance from Colin Keatinge, Sid Verma and David Papadopoulos.