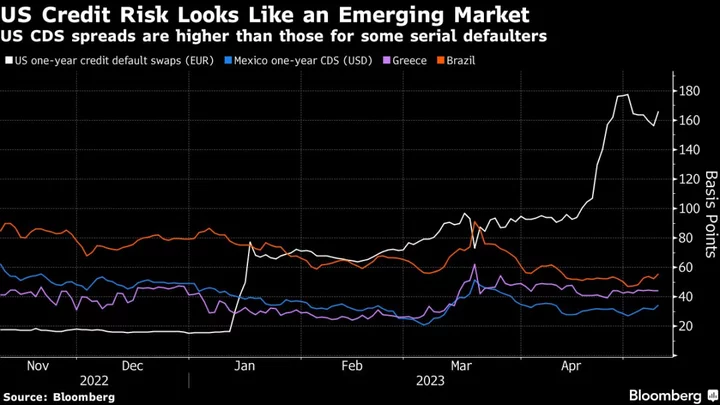

The cost of insuring Treasuries against default now eclipses some emerging markets as the American government gets closer to running out of money.

US credit-default swaps are more expensive than contracts on the bonds of Greece, Mexico and Brazil, which have defaulted multiple times and have credit ratings many rungs below that of the US’s AAA.

Few investors doubt that America will make good on its debts. But even a technical default — one that merely delays interest and principal payments — would roil the $24 trillion Treasury market, the bedrock of the global financial system. For holders of the credit-default swaps, such a scenario would yield a lucrative return.

“There’s something of a gambling going on in US CDS,” said John Canavan, lead analyst at Oxford Economics. “It’s not a pure play that the Treasury will default and remain defaulted. In that sense it’s different from countries like Greece or Mexico, where the concern would be that the government defaults and never pays you back or pays you back with a haircut.”

In the latest twist in Washington, House Speaker Kevin McCarthy reportedly said he opposed a short-term debt-limit extension which would allow the Treasury to borrow through the end of the fiscal year on Sept. 30. President Joe Biden and congressional Republicans made little tangible progress Tuesday toward averting a default, but pledged negotiations on spending that would open the door to a possible agreement.

That came after Treasury Secretary Janet Yellen repeated her warning that the Treasury risks running out of room to stay under the debt ceiling as soon as June 1 — the date when the government exhausts its options to fund itself, commonly referred to as X-day.

The imbroglio has fueled a surge in demand for euro-denominated US credit default swaps, the most actively traded. These contracts against a default over the next year traded at 166 basis points Wednesday, near a record high and surpassing the levels during previous debt-ceiling standoffs in 2011 and 2013.

The trade has taken off due to a derivatives market quirk that will allow holders to reap handsome returns in the event of default. Their payoff will equal the difference between the market value and par value of the underlying asset, an attractive proposition when long-dated Treasury bonds are trading particularly cheap. The potential payout could exceed 2,400%, according to Bloomberg calculations.

“I put some CDX investment-grade protection into my fund last week and will look to add to that position over the next couple of weeks,” said Luke Hickmore, investment director at Abrdn. He’s also reviewing his exposure to US Treasuries, moving towards longer-dated securities.

Hedge Fund Manager Wadhwani Says US Default Risk Worse Than 2011

US CDS are mostly denominated in euros while those on emerging markets tend to be dollar-denominated. But even accounting for that currency difference, insuring exposure to US debt via one-year CDS is several times costlier than in Brazil and Mexico, according to data compiled by Bloomberg.

EM Fallout

Net notional volumes outstanding on US CDS are also now comparable with many larger emerging markets, at $5.5 billion, according to Morgan Stanley analyst Simon Waever. Ironically, emerging markets will be hardest hit by any wider market repercussions.

“History suggests that broader risk assets, including EM sovereign CDS spreads, start reacting a month ahead of the X-date,” Waever said. “That’s a reason to hold off adding EM sovereign credit risk.”

Morgan Stanley Sees ‘Meaningful Risk’ in US Crossing X-Date

The anomaly is limited to one-year CDS. Five-year contracts, which are usually more liquid and better reflect the view on a country’s longer-term credit risk, have also climbed in the US but still trade about 100 basis points below one-year tenors. That inverted curve indicates that risks are seen as more elevated in the immediate future than the longer term.

And most investors remain relatively confident that a technical default will be averted via an eleventh-hour deal, as has been the case so many times in the past.

“The CDS price reflects the cost of insurance on a very big credit in a very small insurance market,” said Charles Diebel, head of fixed income at Mediolanum International Funds. “You can’t translate from the price of the CDS to the likelihood of outcomes.”

--With assistance from Robert Brand.

(Updates to add link to Morgan Stanley note)