China needs to decisively ramp up fiscal spending so it can support an economy damaged by Western restrictions on trade, according to a Chinese scholar studying an unconventional school of economic thought.

Jia Genliang — the co-author of the new book Modern Monetary Theory in China and a professor at the Renmin University of China in Beijing — said China should lift its headline deficit ratio to above 5% of gross domestic product on average for the next decade. That’s more than the 3% level the government has typically adhered to, and even higher than this year’s 3.8% ratio, which was set last month as part of a rare mid-year budget revision to help growth.

Jia’s advice adds to a chorus of economists calling for or predicting the government will roll out more fiscal stimulus to support the economy. Last month’s unusual budget revision and decision to issue another 1 trillion yuan ($138 billion) worth of sovereign debt appeared to many analysts to signal a shift in approach to policy as Beijing grows wary of debt strains on local governments.

Jia is one of the most prominent Chinese proponents of Modern Monetary Theory, whose principle is that countries which borrow in their own currencies don’t face a real debt limit because they can print money to pay for it. That theory has attracted attention in China over the past few years as authorities relied more on fiscal stimulus and infrastructure investment to help a slowing economy.

In Jia’s view, Beijing needs to do more as Western nations including the US maintain curbs on Chinese exports, crimping what has been a key driver of growth over the last several years. He also recommended the government hire more workers and increase public spending to lift residents’ income and consumption.

Here are highlights from a recent interview with Jia, which has been condensed and edited for clarity:

Does China’s economy need more policy support?

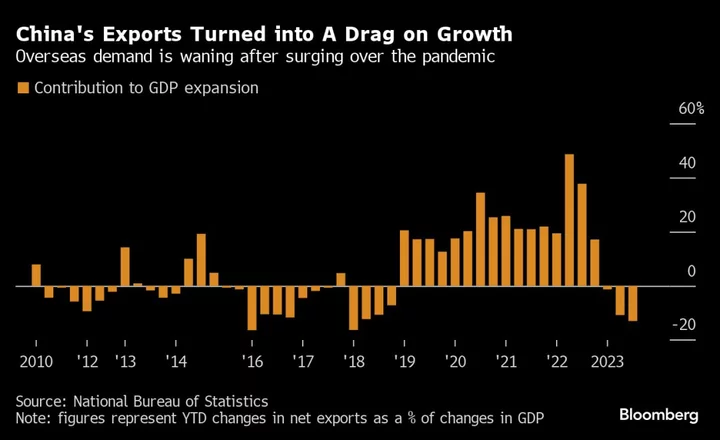

The economy is returning to a downward trend already present before the pandemic. The grim challenge of insufficient demand remains. Exports have been bad this year, and the overall trend is increasingly negative, even though it may improve next year. This is because the widening income inequality in advanced economies has led to a rise in protectionism, which means lower demand for Chinese goods in the long term. China will have no choice but to rely on domestic demand and the domestic economic circulation to achieve growth.

But China is facing a lack of consumption demand, which is fundamentally due to residents’ relatively weak income that fails to absorb products made in the highly-efficient industrial sector. Adjusting income distribution will be a long and difficult process.

I propose a much more direct and effective solution, which is to significantly raise the central government’s fiscal spending — and deficit ratio — to lift residents’ income. That will compensate for insufficient demand and resolve the issue of oversupply.

How do you see China’s external environment as trade tensions rise?

MMT shows us that in a closed economy, the private sector’s net financial assets equals the fiscal deficit. And a trade surplus comes from other governments’ fiscal deficit.

We don’t need to fear even if trade surplus becomes zero, because we can replace exports with a higher fiscal deficit. As the de-globalization trend deepens, other countries are set to implement increasing trade restrictions on China.

China must turn to domestic circulation, and the key is to increase the fiscal deficit to maintain ample capital in private sectors. If we realize this, we will be unafraid of overseas protectionism and Western countries’ containment.

China has the world’s biggest market. We can totally rely on the government’s fiscal capacities and domestic circulation to achieve a medium to high growth again, and usher in a golden era for economic growth.

How do you assess the impact of the government’s decision to lift the budget deficit?

Its greatest significance is that it broke the myth of the “red line” of a 3% fiscal deficit ratio. Setting the ratio at 2.8% last year was an important factor for the economy’s challenges in 2023.

The move to lift the ratio broke a rigid way of thinking, and represents a pragmatic approach. It has led to heated discussion and praise, and had a strong impact on people’s psychology. It will help further break this dogma that has long been abandoned by the international community.

In recent years, China has seen obvious fiscal austerity compared with the US, Japan and European countries. So we still need to further liberate our minds.

What are the most urgently needed policies, in your opinion?

We need to solve the unemployment issue and make wage increases an engine for growth. This requires a job guarantee program that I first proposed in 2020, which can be funded by the central government and organized by local authorities. It will essentially mean the government sets a minimum wage and hires any unemployed workers who are willing to work but couldn’t find a job.

In addition, China needs to resolve the local government debt issue. In the short term, localities should be allowed to issue more general bonds, and the central government should use special sovereign bonds to replace local debt. In the longer term, there should be a reform to the central-local fiscal system.

China also needs to invest in areas such as digital economy, green energy and core technologies, and make them a new growth engine to replace property and traditional infrastructure. We also need to invest strategically in the next industrial revolution in sectors such as nanotechnology, new energy and bioengineering.