Federal Reserve policymakers are increasingly grappling with a critical question: How much should they weigh the adverse impact of their interest-rate hikes on banks against the goal of containing the fastest price increases in decades?

The answer will play a major role in determining whether the Fed is steadfast in keeping rates elevated through year-end as officials expect, or cuts them as traders are betting.

Since US banking turmoil flared in March, the Fed has raised interest rates twice to combat inflation while pumping emergency liquidity into the banking system — discrete actions that underscore officials’ long-standing habit of keeping financial-stability actions apart from monetary policy. The strategy — known as the separation principle — is being tested, as credit-crunch aftershocks threaten to toss the economy into a hard downturn before the Fed has contained price pressures.

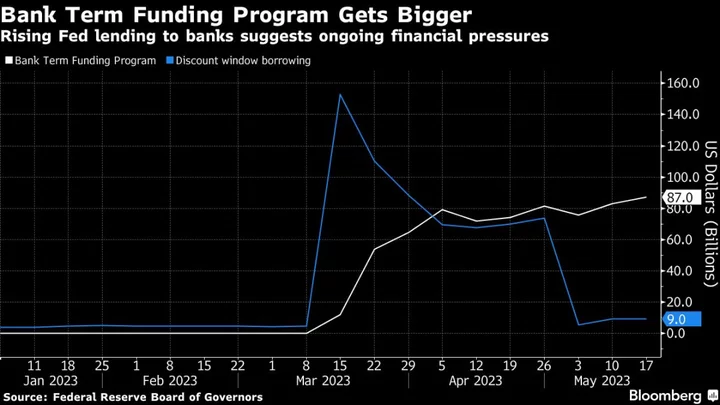

The central bank’s 5 percentage points of rate increases helped trigger the failure of Silicon Valley Bank, the biggest bank collapse since 2008. Since then, the acute stress has eased, but emergency borrowing from the Fed remains elevated, regional bank stocks are down more than 20% this year and survey data suggest lenders are pulling back.

Now, Fed officials are trying to determine what further credit constraints – and the contagion risk from more shaky banks — mean for the economy and inflation, which is still too high.

Fed Chair Jerome Powell on Friday defended the central bank’s two-pronged approach, while acknowledging that the effects are intertwined.

“While the financial stability tools helped to calm conditions in the banking sector, developments there on the other hand are contributing to tighter credit conditions and are likely to weigh on economic growth, hiring and inflation,” Powell told a Fed conference Friday in Washington.

One result, Powell speculated, is that the “policy rate may not need to rise as much as it would have otherwise to achieve our goals.” He also signaled he’s open to pausing rate hikes at the Fed’s June 13-14 meeting so officials can assess the impact on the economy.

The Fed took aggressive steps to try to stem contagion in the financial system in March, including expanding access to its emergency lending programs. Less than a week later, officials went ahead with a quarter-percentage-point rate hike, followed by another in May — both unanimous decisions — despite worries that the turmoil could exacerbate credit tightening that began the previous year.

Higher short-term borrowing costs raise the price banks pay to keep or attract deposits, compressing profits for some. A slowing economy could also make it harder for households and businesses to repay loans.

Ultimately, the Fed’s rate hikes could leave the financial system weaker, making it harder for the central bank to bring the labor market back to full strength, as was the case in the grindingly slow recovery following the global financial crisis.

“There is no economic stability or price stability without financial stability,” said Lou Crandall, chief economist at Wrightson ICAP, who’s followed the Fed for decades. “This has been an unsatisfactory couple of months: FOMC members should think of themselves as central bankers – that is, as stewards of the financial system,” not just inflation fighters.

Financial Risks

The path may not be so smooth. Deutsche Bank economists see risks that financial strains overwhelm monetary policy intentions, though their baseline is that regulators contain them.

“Financial stability risks could forestall further rate increases or even cause the Fed to cut rates if they become severe enough,” they said in a May 12 note to clients. “There could be fundamental reasons for continued banking sector stress that prudential tools may not be able to resolve.”

The KBW Regional Banking index is down 26% year-to-date, while futures traders expect a slowing economy and a wounded financial system to result in rate cuts later this year.

While policymakers initially rallied around the separation approach, unity on the Federal Open Market Committee is starting to fray.

Some Fed officials say it’s hard to quantify the impact of banking stress and more time is needed to see it filter through the economy. A key question is how much damage the banking system may still face.

“The ‘08 experience is burned into me: When every time we thought we were through it, it’s still burning,” Minneapolis Fed President Neel Kashkari said May 11 at an event in Michigan.

“It’s that intersection between how embedded is inflation, therefore what does monetary policy need to do, therefore what strains does that put on the banking sector?” he added.

Other officials say the economic effect is probably small, and see market expectations of a rate cut as misplaced, given how far they are from their inflation goal. The Fed’s preferred price measure rose at a 12-month rate of 4.2% in the latest reading, more than double their 2% target.

“In the current inflationary environment, interventions to support financial stability must not inappropriately ease financial conditions,” Dallas Fed President Lorie Logan said at an Atlanta Fed conference on May 16.

“Even as we consider how best to manage the risks, they must not stop us from doing what’s necessary to achieve 2% inflation,” she said in separate remarks in San Antonio.

Lessons Learned

It’s not clear that Fed officials were paying sufficient attention to “policy-induced risks” that were building up in the system from low interest rates in the aftermath of the pandemic, said former Fed Governor Jeremy Stein.

Stein made the case a decade ago that monetary policy could be used to lean against financial bubbles because it “gets in all the cracks,” meaning it tightens or eases conditions broadly across all forms of financial intermediation.

Fed officials are typically averse to making value judgments about asset prices and using interest-rate policies to affect them. But relying on supervision and regulation to address financial stability risks “is not the world we live in,” Stein said.

“We have learned that lesson over and over again,” he added.

Former Fed Chair Ben Bernanke, who won the Nobel Prize in Economics last year for his work on how financial systems accelerate economic downturns, suggested there’s more to learn about how the Fed’s two sets of policy tools affect one another.

“We really do not understand to the extent that we need to the relationship between different aspects of monetary policy, risk taking, balance sheet behavior,” he said Friday, appearing on the same panel as Powell. “We need to understand much better what the channels are.”