Emerging-market central banks are joining their developed peers in pushing back against expectations of a rapid switch to cutting interest rates, souring the outlook for developing-nation bonds.

Traders have all but priced out the prospect of easier monetary policy in Asia over the next 12 months, paring expectations for lower borrowing costs in Latin America and central Europe, swaps data show. The shift has been driven by the “higher-for-longer” rhetoric from the Federal Reserve, policymakers seeking to support their currencies and the threat of El Niño stoking inflation.

The growing global hawkishness spells more trouble for emerging-market local-currency bonds after traders thought central bankers from richer nations would soon start reducing rates as economies slowed. A Bloomberg gauge of the debt dropped 2% in August, the worst month since February, while an index of emerging-market currencies slipped 1.5%.

“The inflation outlook for emerging markets is becoming less certain, in contrast to the broad-based disinflation of the past four-to-five months,” said Jon Harrison, managing director for emerging-market macro strategy at GlobalData TS Lombard in London. “EM local-currency bonds could also be at risk in the coming months from a further surge in the dollar or more Fed rate hikes, but we are not at that point yet.”

More Hawkish in Asia

A hawkish trend is setting in across Asia. South Korea’s central bank last month pledged to keep policy restrictive for “a considerable time,” convincing traders to price out a full 25 basis-point cut over the next year. Bank Indonesia said earlier in August it would allow short-term bond yields to rise to support the rupiah, adding to signs it’s a long way from shifting to an easing stance.

India’s central bank said last week it’s growing more concerned about surging food prices, prompting the market to pare earlier bets on aggressive rate cuts.

South Korean swaps are now pricing in 8 basis points of rate hikes over the next 12 months, compared with predictions for a tiny cut at the end of June. Indian contracts are anticipating 16 basis points of cuts, down from a chunkier 60 basis points that were priced in on June 30.

“Across regional Asian swap markets, the front-end of curves have gone from unwinding the pricing of rate cuts to now pricing up to a 25-basis-point increase by year-end,” said Duncan Tan, a currency and rates strategist at DBS Bank Ltd. in Singapore.

“While there is probably low conviction among market participants for Asian central banks to hike again, the widening term premium suggests that participants see non-negligible risks of rate hikes starting again,” he said. Term premium is the extra compensation investors require to take on the risk of changing interest rates.

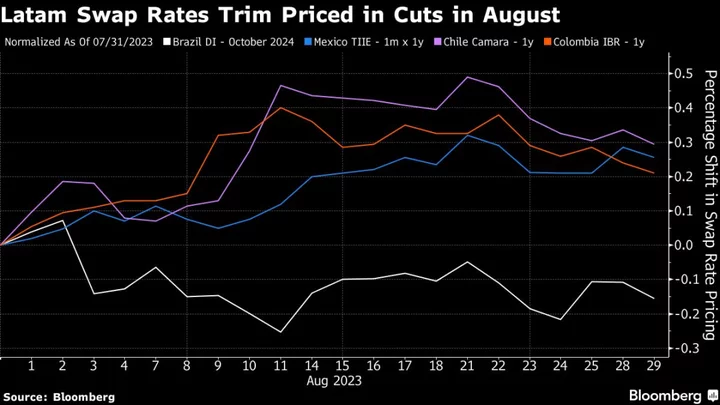

Brazil Exception

Latin America is seeing a similar move toward more hawkish pricing, most noticeably in Chile, Mexico and Colombia. Only in Brazil has the market turned more dovish after the central bank cut its benchmark rate by a larger-than-expected 50 basis points on Aug. 2.

Policymakers in emerging Europe are likewise sounding more hawkish. Czech central bank Governor Ales Michl said last week inflation remained too high, and the discussions at Jackson Hole confirmed the nation’s plan to keep monetary policy tight was the right strategy. Investors shouldn’t assume further cuts will automatically continue, Hungary’s central bank Deputy Governor Barnabas Virag also said last week.

‘Bit of Pain’

Markets may continue to be wrong-footed over the next three-to-six months as they likely view any weakness in data as a sign central banks can cut rates, said Bob Savage, head of markets strategy and insights at BNY Mellon Capital Markets in New York.

“That’s probably how the market’s thinking, and that is absolutely opposite of how almost every central banker wants to think, which is: ‘I want to beat inflation without actually doing anything,’” he said. “The easiest way of doing that is sounding tough and letting the market have a little bit of pain to do the work for me.”

What to Watch

- Inflation in both Thailand and South Korea may have accelerated as the cost of food staples, such as rice, climbed.

- Conversely, consumer price gains in Hungary, Chile and Colombia may have eased from a year earlier.

- Malaysia’s central bank is forecast to keep its key rate at 3%. Polish policymakers are also expected to stay on hold despite double-digit inflation.

- South Africa, Bulgaria and Romania will all publish GDP data.

--With assistance from Davison Santana and Andras Gergely.